CAN YOU HAVE AN EARLY RETIREMENT BEFORE 65?

Today we will explore six scenarios that will allow you to have an early retirement before the age of 65.

I will go through multiple case studies so you can gain perspectives on investing, saving, and retirement before 65 and whether you need to work 45 years, 10 years, or even less than 1 year.

WHAT IS A PENSION?

Firstly, what is a pension?

Typically, you will get a pension deal with the government or your employer.

Usually, it is the average income for the last three to five years, or the best five years of your employment history.

Let’s say you earned $100-150,000 in your last five years. Every year after you’ve retired you would get that amount forever, which sounds like a pretty good deal.

Assuming you do not die for a very long time, how much is your pension worth?

To calculate this, I will first need to introduce you to the concept of annuity. According to The Intelligent Investor book,

“Annuity is insurance-like investments that enable you to defer current taxes and capture a stream of income after you retire… but what the defensive investor really needs to defend against here are the hard-selling insurance agents, stock-brokers, and financial planners who peddle annuities at ridiculously high costs. In most cases, the high expenses of owning an annuity, including surrender charges that gnaw away at your early withdrawal will overwhelm its advantages. The feel-good annuities are bought, not sold. If the annuity produces fat commission for the seller, chances are it will produce meager results for the buyer.”

According to this book, when it comes to investing in an annuity, you are not a buyer so you should only consider buying annuities from providers from rock-bottom costs like Ameritas, TIA, and Vanguard.

Of course, this book is quite old so it may be different nowadays. Nevertheless, I think you can understand what annuity is and it is that you will receive a fixed amount of income continuously, forever.

Typically, we can actually make it more realistic by assuming that this payment lasts 30 to 40 years, depending on whether you are retiring at 60 or 70.

In this case, let’s assume that you want this kind of income forever. You will understand why as we go through the analysis.

Annuity means that (if your deal is entitled to receive $100K) you will receive $100K in year one, year two, year three, so on and so forth.

In this case, I am not adjusting for inflation or any other factors just to keep our model relatively simple.

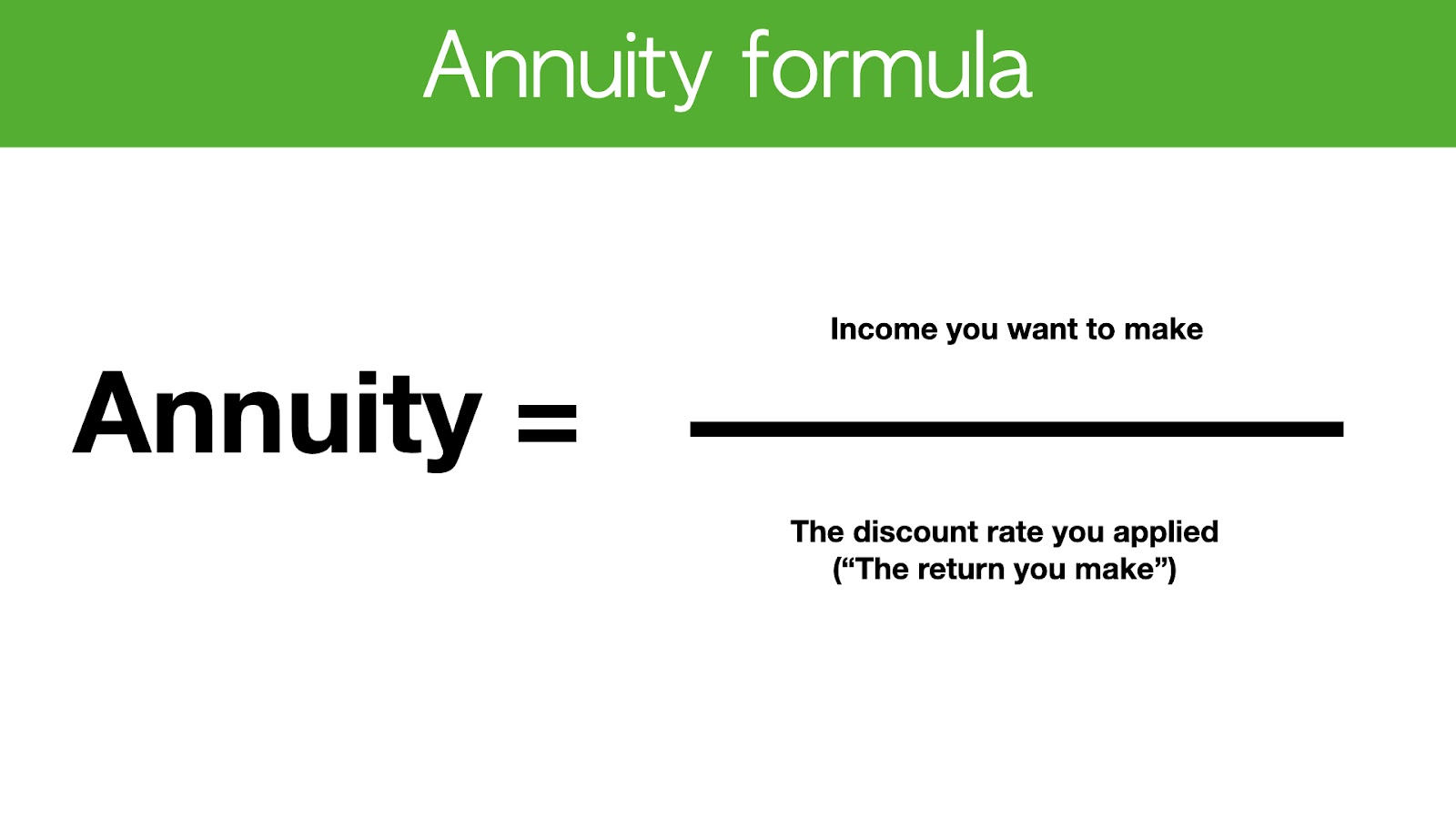

Here is the formula for annuity, to calculate how much this stream of cash flow is worth.

It is actually quite simple. First you take the income you want to make and divide it by the discount rate you want to apply, and the discount rate can be the return that you make.

For example, let’s say that I want to make $100K per year from this pension divided by my return, which is 5% a year. This will give me how much the annuity is worth today which is quite straightforward.

When it comes to investing, sometimes you encounter annuity that is offered by banks or other financial institutions and you can also apply this formula to calculate what the expected return is you will get from annuity.

If your annuity is let’s say $100K or even just $10K per year, then you will take that number and divide it by how much the annuity costs you today so that you can get the interest rates.

That way you will know whether you are getting a good return or not. So let’s jump right into some different scenarios to analyze.

SCENARIO #1:

$100K PENSION AND 10% RETURN

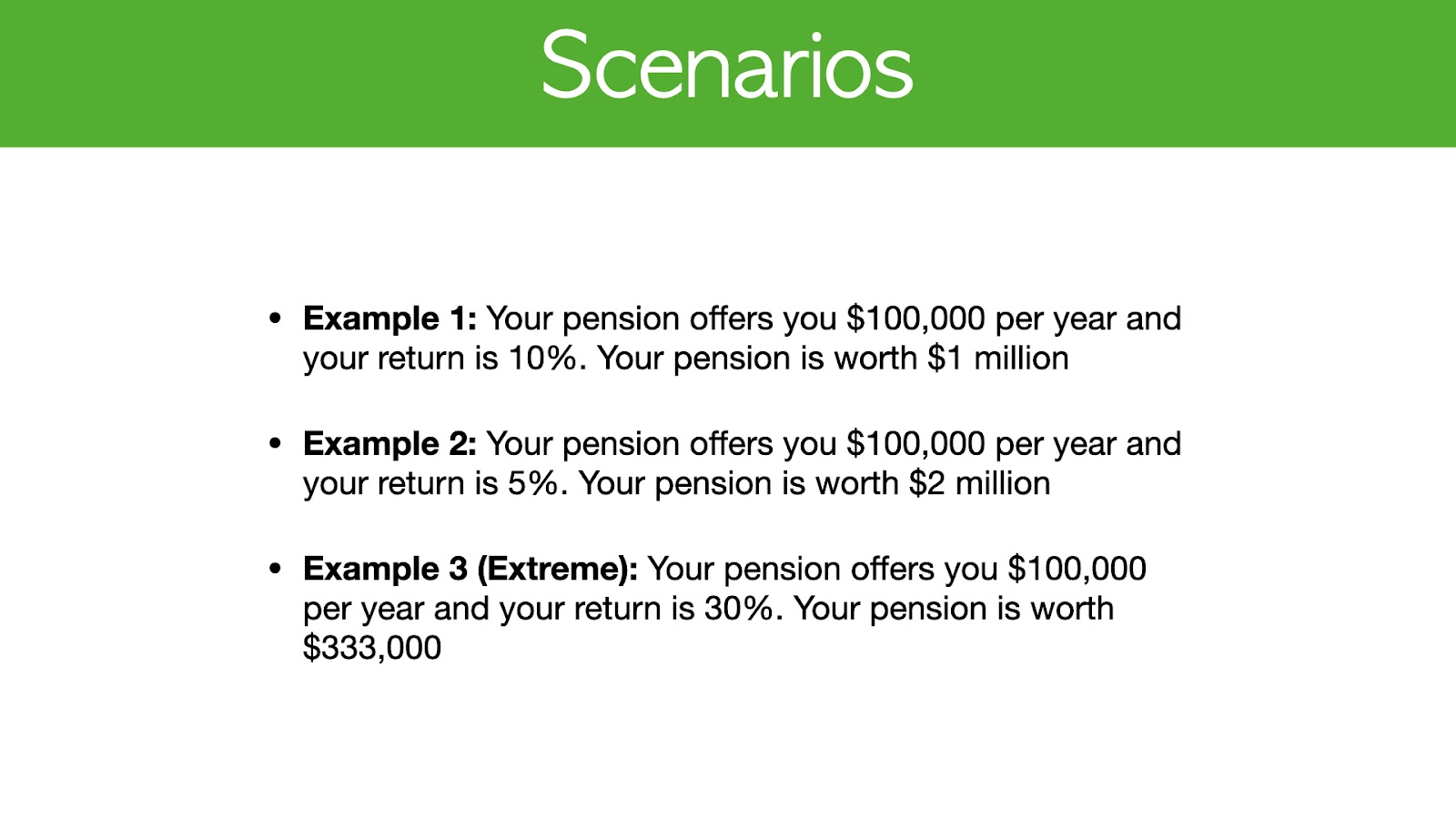

In this scenario, your pension offers you $100K per year and your return is 10%. That means that your pension is worth a million dollars.

I would think that is actually quite reasonable when you consider a lot of people trying to be a millionaire, because once you reach that millionaire status, then you can effectively invest and get $100K per year if your portfolio gets a 10% return every year.

SCENARIO #2:

$100K PENSION AND 5% RETURN

Your pension offers you $100K per year and your return is 5%. This means that your pension is worth $2 million.

For most people, if you are investing in an ETF or in a market and you are getting somewhere between 5% to 10% a year, then when you retire your pension will be worth somewhere between one to two million per year.

This means that whether you are 30, 40, or 50 years old, if you are saving on a monthly basis, you just need to get to one to two million a year. That is the key observation.

SCENARIO #3 (EXTREME):

$100K PENSION AND 30% RETURN

For this example, this is a bit of an extreme case.

Your pension offers you $100K a year and your return is 30%.

This means that your pension is worth $330,000 and as you can see, you are aiming for a 30% return which drastically reduces the size of your pension and the amount of money you need to save to achieve the same level of income.

FOR MOST PEOPLE...

Of course, not everyone in the market can get 30% as it does require additional skills to get to this point.

For most people, your pension is probably going to be worth somewhere between 1 to 2 million so we will go with this assumption and dig a little deeper.

If you do have the skills to earn a 30% return then you will be able to reach your goal faster and that is fantastic. However, in this case we will focus on the general public which is somewhere between 1 to 2 million.

Let’s say you work for 45 years which is our base case in a corporate job or government job.

You take 1 million and divide it by 45 years which gives you $20,000 of savings per year, assuming you earn zero interest and there is zero inflation.

This would be the base case however it is a bit unrealistic because even a bank would give you 0.25% interest. Inflation would be somewhere between 2% to 3% if you are calculating long-term, which means that you would need to save an additional $1,666 in order for you to reach a million dollars in 45 years.

What if you were to make 5% a year?

Most people are going to be working 45 years and your goal is a million dollar pension. If you make 5% a year and you compound this over time, then you are really saving around $6,000 per year.

If you divide $6,000 across 12 months, then that would be $500 per month for 12 months which is pretty realistic and I think a lot of people are able to achieve this.

Now if we look at the higher end and if you were to make 10% a year, this means that you need to save $1,200 a year to reinvest and compound it by 10% over time.

In other words, you’ll have to save only $100 per month which is quite mind-blowing because you will be working for the next 45 years and only have to save $100 a month to be able to retire with a $2 million dollar pension.

If you take a step back and look at the numbers I’ve shown you, it means that in order for you to achieve financial freedom over a period of 65 years, you’re really looking to save somewhere between $100 on the low end to $500 on the high end with a lower return on your portfolio.

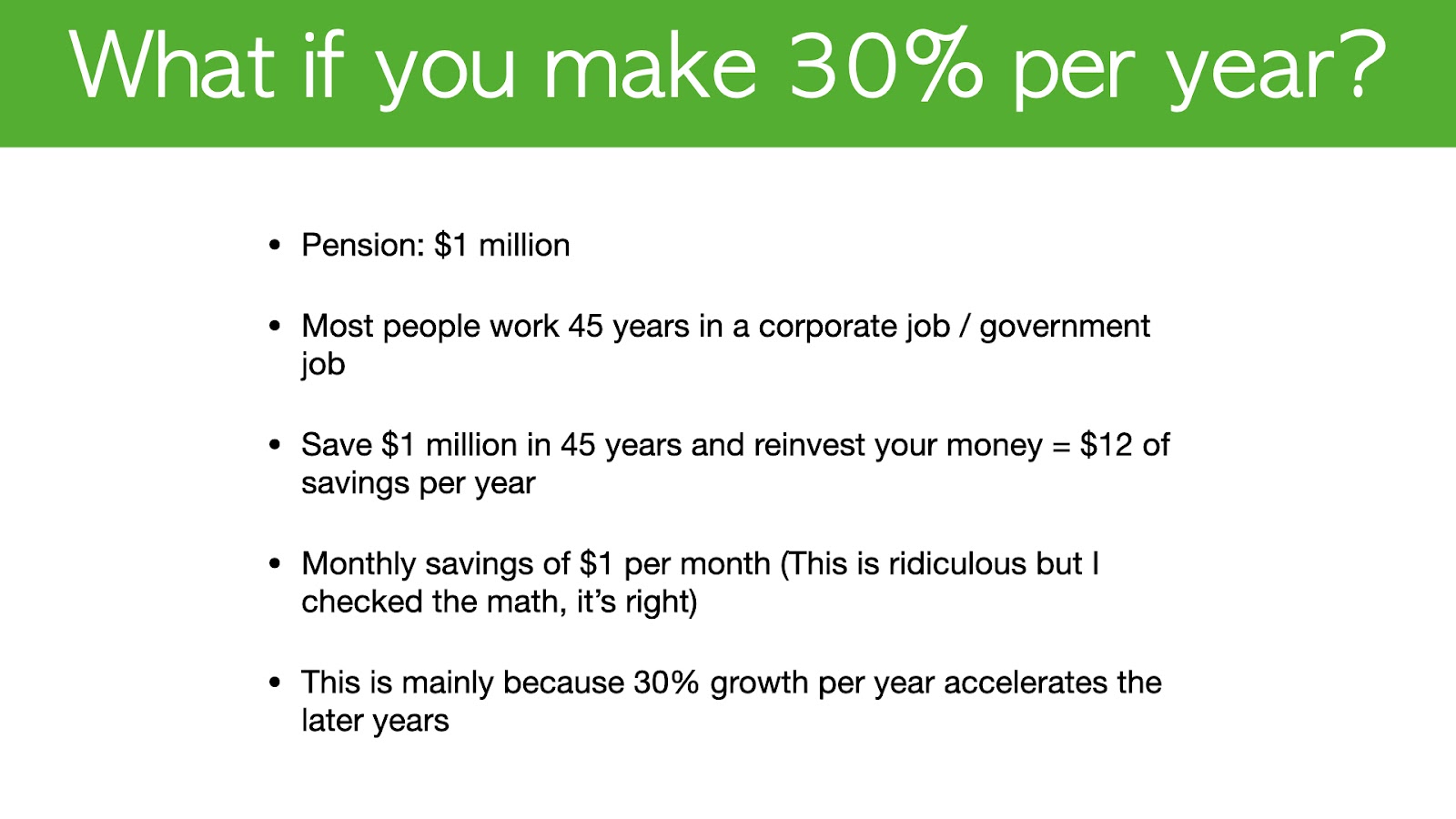

Now let’s talk about a crazy scenario in which you make 30% a year every year.

In this case, if you are able to compound and re-invest this over 45 years, then you will only need to save $12 a year or $1 every month.

When I did this calculation, I thought this was such a ridiculous figure that I had to go back and double check the math.

If are able to compound your portfolio consistently with 30% return over 45 years, it is such a long duration that you will only need to save just $1 a month to achieve this goal.

This is quite unrealistic as who knows if they can consistently achieve 30% every single year and beat the market consistently for 45 years?

So you’ll have to evaluate the likelihood of that happening since you will likely have some bad years as well.

However if you are able to achieve 30% consistently, it allows you to save very little money and still retire because you have 45 years to compound it.

10 YEARS SCENARIO

In these three scenarios, I kept the years constant assuming that you start working at 20 and you want to retire by 65.

However, what if you want to retire as soon as possible?

What if you don’t want to be waiting 45 years slaving away at your day job for that long?

Instead of asking how much money you need to save per month to get to $1 million in 45 years, we should ask what we can do to get to $1 million as quickly as possible, and how long it would take.

EXAMPLE 1:

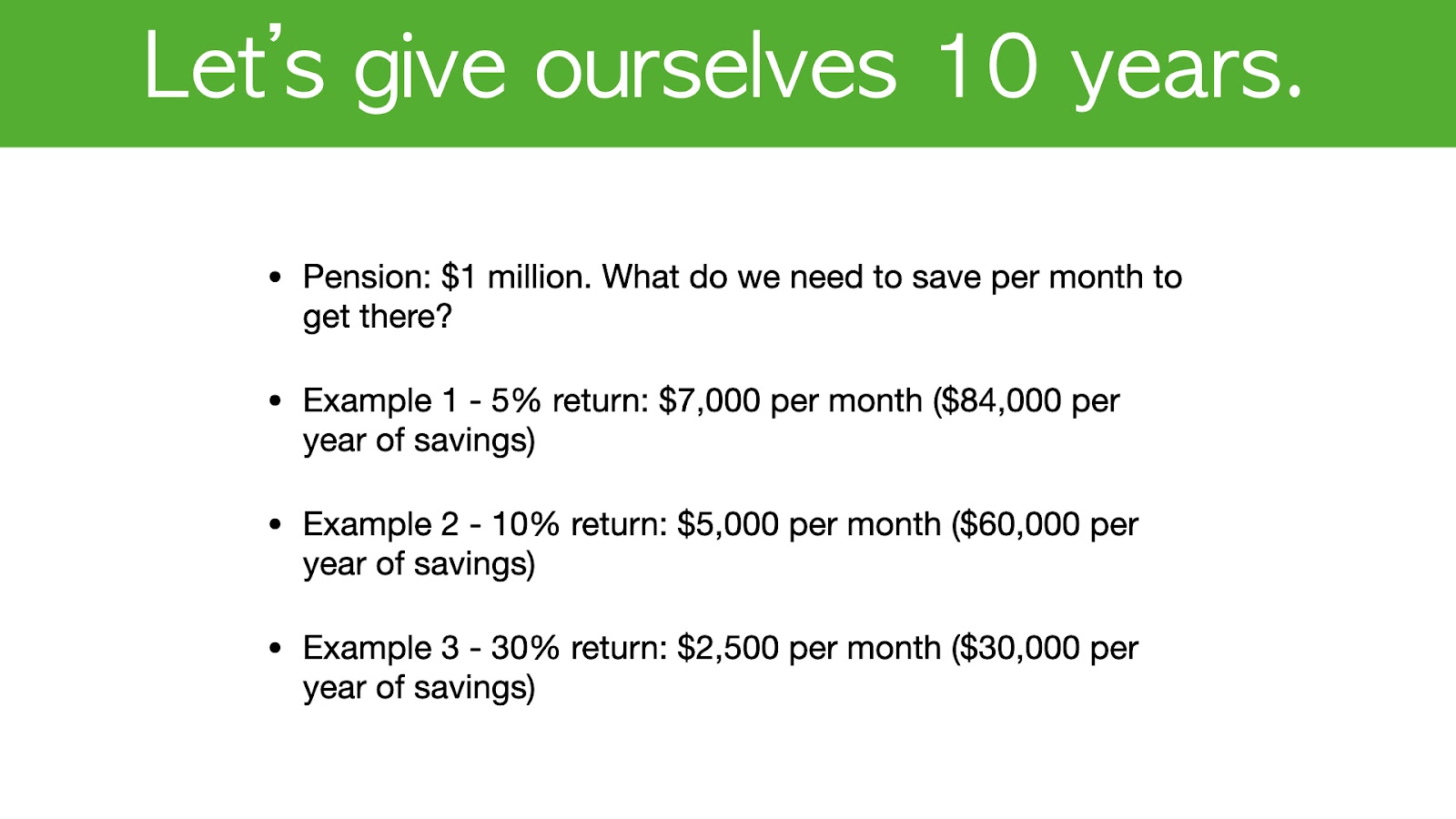

Let’s start with a base case, if you want to retire in the next 10 years. This is perfect for my followers who are 40 or 50 years old.

Let’s say you make a 5% return which is on the lower end. If you are starting from zero today, then you will need to save $7,000 a month every month for the next 10 years to reach that goal, which is a savings of $84,000 per year.

If you think about this map in your head, it makes sense because the return is low. $84,000 times 10 years gives you $840,000 and you add on a little bit in terms of the return.

EXAMPLE 2:

What if you are able to make a 10% return?

In that case, if you are starting from zero today, then you would need to save $5,000 every month for 10 years in order to retire, which is about $60,000 per year in savings.

If you are looking for financial independence and to retire early, then your main focus is to cut your expenses to see if you are able to save your income, a full-time salary, for 10 years to reach $1 million.

Of course, this requires discipline and may mean that you might need to give up something like having kids or having a family, or you need to live at home or whatnot.

That’s really what this method is all about, intense cost-cutting until you can reach your target. However, if you have a family, a full-time job and a lot of things going on in your life such as mortgage payments and car loans, chances are you wouldn’t be able to save $5,000-$7,000 per month.

EXAMPLE 3:

For this example we will examine what would happen if you were to get 30% return.

If you are starting from scratch, you would still need to save $2,500 every month for the next 10 years, which is equivalent to $30,000 of savings per year.

This is drastically lower than if you were to have a 5% or 10% return but still requires quite a bit of discipline for you to save this level of money.

When I am talking about a $1 million pension, you are really looking at $100,000 per year when you are retiring so you would need to evaluate whether that is enough for you and your spouse or just you alone. So what can we explore to reach the path of early retirement?

ENTREPRENEURSHIP

There are some extreme cases where people choose to become an entrepreneur in a few different ways.

For our first example, let’s say you decide to start an e-commerce company.

The average per product is $5 for lower ticket products so you’ll need to sell 200,000 units in a year or however many years to get a million dollars.

If you divide 200,000 by 12, that’s only about 20,000 units a month which is not that bad.

Then you would just have to find some high volume product that will allow you to achieve this kind of volume.

Another option would be to start a software company.

Let’s say the average profit per customer is $200 a month or $2,000 per year.

This means that you will need 500 to 5,000 customers in total.

Some of the businesses that come to my mind include Spotify or MailChimp or hosting services like Netflix or Disney Plus where you offer a subscription model to customers to solve a very specific need. If you have these skills, you can actually consider starting a business.

The third approach is to become a YouTuber where you are looking at about $10 per 1,000 views. To some people this may seem like a stretch but if you have tried getting views on YouTube as I have done, you will realize it’s actually quite difficult to become a big YouTube star.

Nevertheless, you need to reach a hundred million views in order to reach a million dollars. If you look at some popular music videos, it seems like you can achieve that quite easily but if you look like a tiny little channel, you’ll realize that they are miles away from reaching that goal.

If you can think of any other forms of business whether it's a laundromat, restaurant, or insurance company, you just need to calculate what the profit per unit is and use a million dollars divided by that profit per unit to know how many units you’ll need to sell exactly.

Here is where you will realize that success does require hard work and that hard work and knowledge today will save you years into working in the future.

So instead of working 45 years at a corporate job to retire, you might have a better idea on how you can reach that $1 to $2 million pension in a shorter amount of time.

Maybe you can work at your corporate job and save and invest to reach your $1 or $2 million pension, or you can possibly figure out a way to use your creativity and see if you can get there faster. That is the key difference and requires a fundamental change in mindset.

So in this video, I'm going to explore six examples where you can have an early retirement before 65. I'm going to go through multiple case studies at how you can think about investing, saving, and retirement before 65, whether you need to work 45 years, 10 years, or even less than one year now, 96.4%. So if you guys have not subscribed yet, and it is free and you can always change your mind in the future. And in terms of this month, I am looking to help 20 full-time professionals without a financial background to master investing and investing a celebrator. And the stretch goal is 30 people. So let's talk about whether you will get an early retirement before the age of 65. Well, first dive into the question of what is a pension. And typically you'll get a pension deal with a government or your employer.

And usually it goes something like this is the average income for the last three to five years. Usually it is the best five years of your employment history. So let's say you make a hundred thousand to 150,000 in your last five years. And every year you retire, you get that amount forever. It sounds like a pretty good deal. So assume you don't die for a very long time. How much is your pension worth? So to do that, I'll need to introduce you to the concept of an annuity. So let's see if the book intelligent investor talks about annuity and talks about inflation history, defensive investor, the negative approach. It doesn't really talk about the annuity. There's no annuity all. And I stand corrected. It talks about annuity page 110. Here is Benjamin Graham's view on annuity. An annuity is these insurance investments enable you to defer current taxes and capture a stream of income after you retire.

But what the defensive investor really needs to defend against here are the hard selling insurance agents, stock brokers, and financial planners who peddle annuities at ridiculously high costs. In most cases, the high expenses of owning an annuity, including surrender charges back now away at your early withdrawal will overwhelm its advantages. The feel good and equities are box not sold. If an annuity produces fat commission for the seller, chances are, it will produce meager results for the buyer. And when it comes to investing in an annuity, you aren't a buyer. So you should only consider buying a new cities from providers from rock bottom costs like Ameritas, Tia, and Vanguard. So obviously this book is old, so it might be different nowadays. But nevertheless, I think you get what an annuity and annuity is that you will receive a fixed amount of income continuously forever. Now, typically we can actually make it more realistic by assuming this payments to be around 30 years or 40 years, depending on whether you're retiring at 60 or 70.

But in this case, we're just going to assume that you want this kind of income forever. And you understand why as we go through the analysis. So what an annuity means is that in year one, you'll get a a hundred K in year two, you'll get a hundred K year three, a hundred K so on and so forth. And in this case, I'm not adjusting for inflation or whatnot. So to keep our model relatively simple. So here is the formula for annuity to calculate how much this stream of cashflow is worth. And it's quite simple. Actually, you take the income. You want to make divided Ida discount rates you want to apply. And this discount rate can be to return. You make, for example, let's say I want to make a hundred thousand per year from this pension divided by my return, which is 5% a year.

That will be how much the annuity is worth today. Quite straightforward, right? It comes to investing. Sometimes you encounter annuity are offered by banks or other financial institutions, and you can actually use the formula. I just taught you to calculate what is the expected return that you'll get 40 annuity. And let's say your annuity is a hundred K a year or even just 10 K a year. So then you take that and divide it by how much the annuity costs you today so that he can get the interest rates. So that way you will know whether you're getting a good return or not. So we're going to go through a couple of scenario analysis. The first one is your pension offers you a hundred thousand per year and your return is 10%. So that means your pension is worth a million dollars. So I would think that is actually quite reasonable when you consider a lot of people trying to be a millionaire, because once you reach that millionaire status, then effectively you can invest and get a hundred thousand a year.

If your portfolio is 10% a year. So example number two, your pension offers you a hundred thousand per year and your return is 5%. So that means your pension is worth $2 million. So that means for most people, if you're investing in an ETF or investing in a market, and you're getting somewhere between 5% to 10% a year, when you retire, your pension is worth somewhere between one to two millions a year. So that means whether you're 30 years old, 40 years old, 50 years old, and you're saving on a monthly basis. You just need to get to one to 2 million a year. So that is one of the key observation. And here is a third example, which is a little bit extreme. That's your pension offers you 100,000 a year and your return is 30%. And that means your pension is worth $330,000. So as you can see, if you're aiming for a 30% return, and that drastically reduced the size of your pension and the amount of money you need to save to achieve the same level of income.

But of course not everyone in the markets can get 30% and it does require some additional skills to get there. So for most people, your pension is probably going to be worth somewhere between one to 2 million. So we're going to go with that assumption and dig a little bit deeper. And of course, if you know how to get 30% return a year, then of course you will reach your goal faster, which has fantastic. But in this case, we'll focus on the general public, which is somewhere between one to 2 million. Now let's say you work for 45 years, and that is our base case in a corporate job or a government job. So you really take that 1 million divided by 45 years. And that is $20,000 of saving per year. And that assumes you earn zero interest, zero inflation. So this is really the base case is a little bit unrealistic because even a bank will give you like 0.25 interest. And the inflation is somewhere between two to 3% when it comes to long-term inflation. So that means you'll need to save $1,666 in order for you to reach a million dollars in 45 years. So that is the base case. And if it is not clear, I just basically talk 1 million divided by 45 years.

So what if you make 5% a year, most people are going to be working 45 years and your goal is a million dollar pension. So if you make 5% a year and you compounded over time, then you're really saving around $6,000 per year. So if you divide it by $6,000 across 12 months, then that would be 500 a month for 12 months. So that is pretty realistic. And I think a lot of people can actually achieve that. Now let's be a little bit more aggressive and look at the high end. What if you make 10% a year, so same calculation, except we increased the return. So that means you need to save 1,200 a year reinvest and compound it by 10% over time. So that's only a monthly saving of a hundred dollars a month. So when you think about it, wow, given us, you will be working for the next 45 years or whatnot.

You can just save a hundred dollars a month and you'll be able to retire with a million dollar pension. So that means if you save $200 a month and you will be able to retire with a $2 million pension, which is near the high end. And when you take a step back and think about the numbers I just showed you, it means that in order for you to achieve financial freedom over a period of 65 years, you're really looking to save somewhere between a hundred dollars, which is on a low end to $500, which is on a high end with a lower return on your portfolio. Now let's do a crazy scenario. What have you make 30% a year? And in this case, if you are able to compound and re-invest over 45 years, so you just need to save $12 a year, which is $1 a month.

When I did the calculation, I thought to myself, wow, this looks ridiculous. So I need to check the math. So I went ahead and checked the math. And that is really because if you compound your portfolio consistently with 30%, over 45 years, because it is such a long period of time that even if you just save $1 a month, you will be able to achieve that goal. This is a little bit unrealistic because who's going to be saving $1 a month. First of all. And second we're saying that you can achieve 30% every single year without fail for 45 years, which means you beat the market every single year for 45 years. So you can think about that and evaluate the likelihood of that happening. They aren't going to be some good years and some bad years as well. And a 30% growth really allows you to save very little money and still retire because you have 45 years to compound it.

So, so far the three versus three scenarios I went through, I kept the years constant. I assume you start working at 20 and you want to retire by 65. So you worked for 45 years, but what if you want to retire as soon as possible? What if you don't want to be waiting 45 years and slaving away on your day job for so long. So instead of asking how much money do you need to save per month to get to 1 million in 45 years, we should ask what we can do to get to 1 million as fast as possible. And how long would it take? So let's start with a base case. And we look at wanting to retire in the next 10 years. And this is perfect for my subscribers that are 40 years old or 50 years old, where you're looking to retire in the next 10 years or so.

And let's say you make 5% return, which is on the low end. If you are starting from zero today, then you will need to save $7,000 a month every month for the next 10 years to reach that goal. And that is $84,000 of saving per year. And if you think about the map in your head, it kind of makes sense because the return is low. So if you take 84,000 times, 10 that's 840,000. So you add on a little bit in terms of the return. So the math checks out now, what if you're able to make 10% return? And in that case, if you're starting from zero today, then you would need to save $5,000 a month every month for the next 10 years in order to retire. So that is $60,000 per year of savings. And that is why when you're looking at the financial independence and retire early fire community, they always focus a lot on cutting your expenses, because you can see if you are able to save your income, which is basically a full-time salary, just save it for 10 years.

You will be able to reach a million. Now, of course, that takes a lot of discipline. And that means you might need to give up something like having kids or having a family, or you need to live at home or whatnot. But that's what the community is all about is intense cost cutting to the point where you can save until you hit that target. Now, in this case, if you have a family, if you have a full-time job and you have a lot of things going on in your life like mortgage payments or car loans, chances are you wouldn't be able to save 5,000 to $7,000 per month. Now let's look at a third example, which is more extreme 30% return. Now, in this case, if you're starting from scratch, you would still need to save $2,500 per month, every month for the next 10 years.

So that is $30,000 of savings per year. So this is drastically lower than 5% and 10% return, but still, it requires quite a bit of discipline for you to save this level of money. And when I'm talking about a million pension, you're really looking at a hundred thousand dollars per year when you're retiring. So you need to evaluate whether that is enough for you and your spouse or just you alone. So let's think about ways where you can explore the path to retirement faster. So that actually brings me to the concept of entrepreneurship. So when you think about some extreme cases where people choose to become an entrepreneur, there are a couple of ways you can do it. So let's say you are starting an e-commerce company. And the average per product is $5. I'm looking at lower ticket products. So you'll need to sell 200,000 units in a year or however many years to get a million dollars.

So when you think about it, Hey, maybe it's not that difficult to sell 200,000 units, because if you take 200,000 units a year divided by 12, so that's what only 20,000 units a month. So then you just need to find some high volume product that you can achieve this kind of volume. The second option is really starting a software company. And let's say the average profit per customer is 200 a month or 2000 per year. So that means you'll need 500 customers to 5,000 customers in total. Some of the businesses that came to my mind, including Spotify or MailChimp or hosting services or Netflix or Disney plus, where you're offering a subscription model to customers to solve a very specific need. So if you do have these skills, you can actually consider starting a business. The third one is really being at utuber and here you are looking at what, but basically you get somewhere along the lines of $10 per a thousand views.

So to some people, this might seem like a lot to some people, it might seem like not a lot, but if you have tried getting views on YouTube, like what I'm doing right now, you will realize it's quite difficult to become a big YouTube star. But nevertheless, it means that you need a hundred million views in order to reach a million dollars. So if you look at some music video, then Hey, you can achieve died quite easily. But if you're looking at my tiny little channel, then you'll realize that I'm miles away from reaching that goal. So you might think, Holy cow, Eric is never going to get there, but that's not the purpose of this channel. If the purpose of this channel is to teach you investing. And if you can think of other forms of business, whether it is a laundry mat, whether it's a restaurant, whether it is insurance company, you just need to calculate what is the profit per unit, and then use a million dollars and divided by that profit per unit.

So then you can know how many units you need to sell. And here's where you realize that success does require hard work and hard work and knowledge today will save you years into working in the future. So instead of working 45 years at a corporate job to retire, you might have a better idea on how you can reach that million dollar to $2 million pension in a shorter amount of time, because let's say today, you don't have a job. And he asks herself, okay, would I radical work at a corporate job for 25, 35, 45 years to reach a million chameleon, $2 million pension, or would I rather figure out a way, use my creativity and see if I can get to a 1 million to $2 million faster. So that is really the key difference, and that is a fundamentally change in mindset. So when it comes to investing in planning for retirement, my goal is really to make 30% a year.

And that's why in this video, I made a couple of examples where I talk about getting to the pension amount, using 30% return a year, which allows me to get there faster and also in a shorter amount of time and also save less money. So if you're interested in knowing how I get a higher return in the markets, then you can get the four hour free case study that is on my website. So this is perfect for you. You are a full-time professional without a financial background. You want to retire early and you want to manage your own portfolio as well. So the link is down below it's five minute investing.com/free case study. So you can graph the training into the description in terms of some of the students that have helped in the past here, you can see that Erin made 16% from CAE and airline related company in four weeks.

Andy made 35% from ADP in three months. And Mike made a 78% from ADP 60% from CAE and 19% from Southwest airline as well. So congratulations to Erin, Andy and Mike, these are a fantastic return and that will help you get to retirement faster. So in terms of the giveaway for this video, I'm going to be giving away one of my favorite books, the one thing, the surprising, simple truth behind extraordinary results. So if you want this book, then just gently tap the like button, leave a comment below. And once we reach a hundred likes, I'll pick a winner and for a previous giveaway for rich data and pour that at the book, I have selected George as the winner, George, if you're watching this video, make sure to reach out to me. I have left a comment on exactly how you can redeem this book for that video. So congratulations, George, for the next video, I'm going to talk about an update on wall street, buys me a Tesla series and how the portfolio is doing and what is the new investment I've made. So I'll see you in the next video.