Today's topic:

Does investing frequently actually increase your taxes?

Does it mean you will need to work harder to pay for additional taxes that you incur?

How much harder do you need to work when it comes to investing to pay for the taxes?

In this series, you will learn how to calculate capital gain tax, how much tax is required to be paid by a dividend investor and a capital gain investor, and also how much tax you will need to pay if you are investing frequently.

LONG-TERM CAPITAL GAIN TAXES

The analyses of trading frequency will be centralized around long-term capital gain taxes, in which you are only paid when you exit.

The rule of thumb for taxes in Canada is 25%, while for the US it is anywhere between 15-25%, depending on the state you are living in.

I have created two scenarios to paint the picture of what happens when you invest often over the course of ten years.

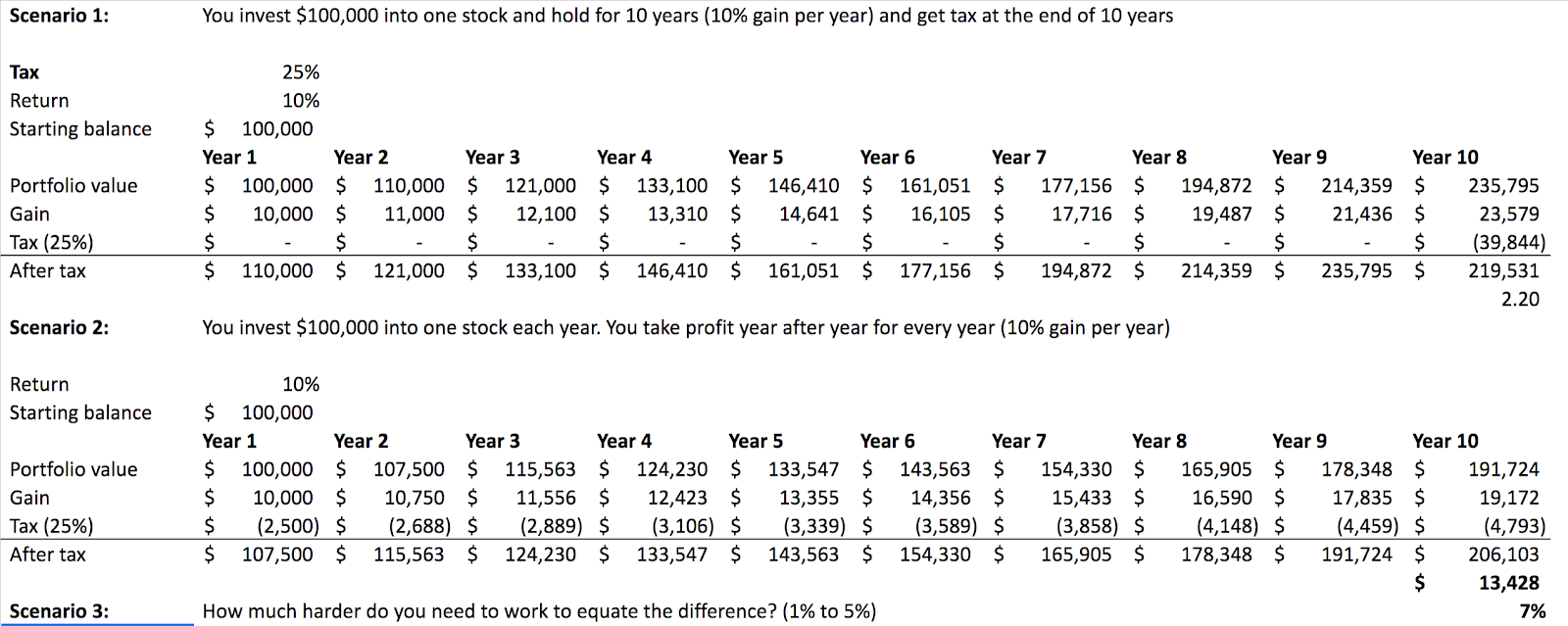

The first scenario is that you invest $100.000 into one stock and hold onto it for 10 years.

You do not incur any tax in between the first 9 years, and only take profits at the end of 10 years.

This scenario paints the picture of the lowest possible trading frequency, in which you are only taxed once.

In scenario two, you invest into a new stock every year and also exit and take profits every year. This means that over the course of ten years, you are also being taxed ten times every time you take profits.

INVESTING FREQUENTLY VS. INFREQUENTLY

I have created an excel spreadsheet so you can visually compare the two scenarios and understand what happens when you invest frequently.

SCENARIO 1: INVESTING INFREQUENTLY

In the first scenario, you invest $100,000 into a single stock and hold onto it for 10 years.

You get 10% each year and you are only taxed once at the end of the 10 year period. Tax is about 25% and your return is 10% to begin with.

These are the initial values for scenario 1. As you look over the years, you are gaining and compounding over the 10 years and do not incur any taxes until the very last year.

The way this is calculated is that you actually sum up all the gains because this is how the Canadian and US government does it, then times it by the tax rates.

At the end of ten years, you pay $39,844 in taxes and your total portfolio value is $219,531. This is a total return of 10% over time or 2.2x of your return, which is fantastic.

SCENARIO 2: INVESTING FREQUENTLY

In this scenario, you invest into one stock each year. You take profits year after year every year, and still get 10% gain.

In this case, you can see that the formula changes from scenario 1, so that you get taxed every year. In the first year you are taxed $2,500, and in the second year you are taxed $2,688.

You are taxed slightly more every year until the 10th year, and as a result your portfolio is actually reduced by a little every year.

This method actually slows your growth down.

At the end of ten years, your portfolio value is $206,103. This means that by investing and taking profits every single year, you will have to pay $13,000 more in taxes.

This is the true cost of investing more frequently, by looking at taxes alone. Take into consideration that this calculation does not include transaction fees or any other fees.

With these calculations, this is a 7% change in your entire portfolio.

This is the formula for comparing the two methods.

When you think about a $13,000 difference over the time span of 10 years, that is approximately $1,000 more per year.

If you want to be more active and manage your own portfolio, then you need to perform better by earning an extra $1,000 per year.

This is only a 1% difference, which is not really a stretch goal. For example, if I change the return to 11% in scenario 2, even if you are exiting once a year you will still be able to achieve the same return even after taxes.

WHAT ABOUT A 30% RETURN?

Here is another interesting scenario.

If you are making 30% a year, how would that impact this calculation?

If I change the figure for scenario 1 to a 30% return instead of 10% you will see that you will owe 10 times more in taxes, which is what my plan is.

The amount of tax you pay at the end is $319,646 which is quite a hefty sum.

What would happen then, if I change this figure in scenario 2 from 10 to 30% as well?

You can see that the portfolio grows from $100,000 to $760,000.

This is a difference of about $300,000.

When comparing the two portfolios at 30%, scenario 1 is at $1,000,000 and scenario 2 is at $760,000.

This means that by investing frequently, you actually need to work harder and pay $297,000 more in taxes.

When you think about this balance relative to your portfolio, it is a difference of 39% which is actually quite significant.

If you are going to make more moves and invest more frequently in the market, then you should also be prepared to pay more taxes over time and be aware of taxes slowing your portfolio growth.

Stay tuned for the next post where I will tell you why delaying investing is costing you $300,000 and what you can do about it.

This will be a very interesting topic because most people misunderstand the true cost of procrastination and the true cost of delaying investing.

So does investing frequently actually increase your taxes? Does investing frequently means you need to work harder to pay for the additional tax that you incur and how much harder do you need to work when it comes to investing and paying taxes. And that's what this video is about. So before we start, 96.4% of you guys are actually not subscribed yet it is free and you can always change your mind in the future. And have you stayed till at the end of the video, then you'll also know about the giveaway. Now this is really part of a larger investment tax series, where I cover how to calculate capital gain tax. How

much tax do you need to pay as a dividend investor and a capital gain investor, and also how much tax do you need to pay if you are investing frequently? So in terms of success stories, I just want to celebrate another success story within investing accelerator, where Daniel made 150% from FedEx in 7.5 months. So congratulations, Daniel, you're doing an amazing job. And this is the 94th case study in investing accelerator. So this month I'm looking to help 20 professionals without a financial background to master

investing and target 30% a year. And a stretch goal is 30 people. So you'll get more details about this at the end of the video as well. So to think about trading frequency and investment taxes, I actually prepared a 10 year Excel worksheet to analyze this problem. And before we dive in, I just want to reiterate that the longterm capital gain tax is what we're going to focus on. And you only paid us when you exit. So the rule of thumb for Canada is 25%. Long-term capital gain. While for us is somewhere between 15 to 25%, depending on the States you're living in. So let's get started. So the first scenario I'm

going to cover is that's. If you invest a hundred thousand dollars into one stock and you hold it for 10 years, so you don't incur any tax in between the first nine years, and you only take profits at the end of 10 years. So this is probably the lowest trading frequency. You can get, you get tax once. But scenario number two is that's. You invest into one stock each year and you take profit every single year. So then you take profits 10 times. So in that scenario, you actually get taxed 10 times. So the question we're trying to answer here is if you are taking profits more frequently, do you need to work harder and exactly how much harder do you need to work and whether that is worth it. So here you will see the Excel sheet that I have prepared. And for the first scenario, you will see that you invest a hundred thousand dollars into one stock and hold for 10 years and you get 10% each year and you get tax at the end of 10 years. So the tax is 25% and a return is 10% and you start with 100 K. So these are the initial inputs. And as you can see, as you are making gain and compounding over the next 10 years, you actually don't get taxed at all until the very last year. And the way this is calculated is actually you sum up all of the gains because

that's how the Canadian or the us government does it. And then you ties it by the tax rates. So then you pay tax of 39,844 at a 10th year. Your total portfolio value is $219,531. So you can see that's overtime making 10% return. This is approximately two point something X. So this is actually 2.2 X of your return. So that is fantastic. And you pay $39,000 in taxes. Now, what if scenario two, you invest into one stock

each year. You take profits year after year, every year, and you still get 10% gain. So in that case, you'll see that the formula here change where you get taxed every year. So the first year is 2,500. The second year is $2,688. And you keep going until the 10th year. Your portfolio is actually reduced slightly every year. So this actually slows your growth down a little bit. And right now, if you just go to the end and look at the difference your portfolio value at the end of 10 years for scenario two is 206,000 $103. So that means by investing and taking profits every single year, you need to pay $13,000 more in taxes. So this is really the true costs of investing more frequently, looking at just taxes alone. We haven't considered transaction costs or anything like that. So when you try to calculate your change in portfolio, this is 7% of your portfolio. I just showed you the formula there. When you think about that across 10 years, you only need to pay 13,000 more in taxes. That's approximately 1000 more per year. So that means if you want to be more active, if you want to manage your own portfolio, then you need to perform better than if you're leaving a loan by $1,000 a year. So that is 1%. And when you think about it, it is not really a stretch goal. So if I change this return to 11% and you'll see that this basically reduces the difference significantly to almost zero is negative 1% now. So that means if you are able to achieve the 11% instead of 10% per year, by actively managing it even exiting once a year. Now, here is another interesting scenario. What if you are making 30% a year, how would that impact this calculation? So I'm going to change the two return figures here. So den is 30% is up top. And in this case, you'll see down to this almost 10 times after tax, which is what my plan is. And the amount of tax you pay is actually $319,000, $646. So when you think about that, okay, that is a hefty sum to pay near the end. So what would happen if I changed this 10% to 30% for scenario two as well? So I'm going to change that. And here you'll see that the portfolio will grow from a hundred thousand dollars to $760,000. So when you think about the difference is Ashley 300 K. So when you compare to two portfolios, one is at a million and the other one is 760 K. So that means by investing frequently, you actually need to work harder and pay $297,000 more in taxes. And when you think about this balance relative to your portfolio, that is 39%. So that is actually quite significant. So that means if you are going to make more moves or investing more frequently in the market, then you'd be better prepared to pay more taxes over time, because it does slow down your return because there's 25% is pretty hefty when it comes to investing. My goal is really to make 30% a year. And when I first started, this seems like a stretch goal to me is like going to Mars. That's why I prepared a four hour free training for you to explain how I did it, the thought process that I've gone into it, and also walk you through a couple of example analysis as well. So this is perfect for you. If you are a full-time professional with no financial background, and you want to learn how to manage your own portfolio, and you want to get a higher return than 10%, which is what you get from mutual funds and index funds. So you can go to the first link below, which is five minute investing.com/free case study to attend to free training and make sure you grab a cup of coffee or even two cups of coffee. Before you start throughout that investing journey. I started coaching other people as well. And that's where Daniel made 150% from FedEx in 7.5 months. So he's the 94th case study. So congratulations, Daniel. And this month I'm looking to help 20 professionals without a financial background to master investing and target 30% a year. So the stretch goal is 30 people. So if you're interested, go attend to four hour webinar, and then we can have a chat, which you will find a link below as well in terms of the giveaway. I'm going to be giving away and not, or copy of Sam Walton made in America, which is his own biography and is a really good read. So if you haven't read this book and you want to learn more about business, what makes Sam successful? What makes Walmart successful? Then this is the right book for you. I have underlined read through this book multiple times. So is definitely one of my favorites. Now in terms of a previous giveaway where I gave out harmonic trading, it's a technical analysis book done can, is the winner. So I've sent you the details on how to contact me and how to redeem this book. So if you're watching this video, make sure you go back and send me your details. So in the next video, I'll talk about why delaying investing is costing you $300,000 ad, what you can do about it. So that's a very interesting topic because most people misunderstood the true costs of procrastination. Most people misunderstood the true cost of delaying investing. So I'll see you in the next video.