In this video 2 TIPS to Retire Faster: achieve escape velocity in the rat race. You will learn about concepts to target your retirement balance and how much buffer do you need in order to live a comfortable life.

Grab the free tool "Retirement Planning and Return Calculator"

Eric here. Where should I send it?

Why is it important for retirement?

Escape velocity is the speed in which a rocket needs to achieve in order to escape from Earth.

The scientific definition is that it has two variables, the mass and distance to the center of Earth. You want to use this concept for retirement.

For Earth, it is 11,186 meters per second.

When you look at this specific number, it makes you wonder, is there a specific number you need to achieve in order to escape the rat race and your nine-to-five job? I’m gonna help you calculate that number.

On reddit, there’s actually a community for people who want to achieve the this concept of retirement and it is called Financial Independence and Early Retirement.

What is the formula for escape velocity for wealth?

")

It is a function of the size of your portfolio or the size of your account times the return you get. This is the formula for the retirement escape velocity. Your account balance times the return you get annually, which needs to be greater than your expense per year.

Here’s a scenario to help you calculate your retirement escape velocity

If your money is just sitting in a bank and it's making 10%, then it's gonna be quite difficult for you to retire. But if you have a high return and a large balance, then it's easy for you to retire.

So if you wanna retire faster, then you need to make a higher return, which requires a more complicated strategy, and requires you to have more knowledge when it comes to investing.

Step #1: Determine Annual Expense

For most people, your annual expenses is really looking at around $80 to $100K or so.

Whenever you start saving money and it starts compounding, then from that day onward and 15 to 17 years down the line, you will be able to retire with a million dollar portfolio.

This is really why so many people are fixated on becoming a millionaire, because if you hit a million and you earn 10% a year, that is sufficient to cover your family's expenses.

Step #2: Determine Annual Return needed to cover your expenses.

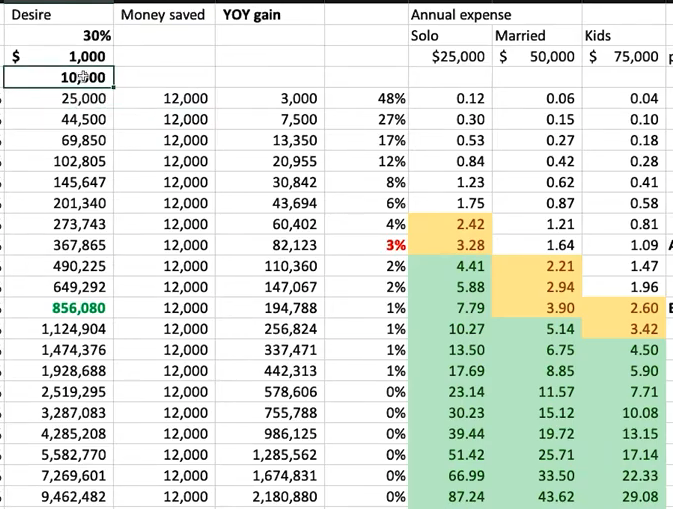

This is a scenario analysis for myself. When I first started, I started with very little money. I started with like $10K and I was saving around $1000 a month, I was able to make 30% a year.

If I want to achieve escape velocity, initially I'll be saving $12,000 a year. If you take a look at Line 1 in the graph below, this actually doubles my portfolio from just saving money alone.

Here is a chart that lists Earnings, Expenses, Money Saved, Year Over Year Gain, and Portfolio size and growth.

If I have a small portfolio and I save $1,000 and make 30%, I can already retire and cover my expenses of 40K with a $200K portfolio (row 6).

If I want a little bit more buffer room then I will need a $300K portfolio. In year 7 (Row 7), and I would have a $60K year-over-year gain.

Step #3: Determine how much you need to save and when to stop saving

From row 7 onwards, you can already see that my saving of $12,000 doesn't really contribute much anymore. You can see that it makes a less significant contribution to my portfolio, constituting only about 4% increase.

After a few years, the impact of savings gradually drops to zero afterwards, so it's not really useful to save that much money after you have achieved what I called critical mass, or the minimum amount required to launch escape velocity.

You'll see that this number actually goes down over time because as your portfolio grows and grows, the saving factor actually doesn't impact your portfolio growth as much.

So saving is really important in the first five to seven years. But once you reach a certain portfolio size, and in this case, $367,000, then the saving of additional $12,000 ($1000 per month) doesn't really move the needle, it only amounts to 3% of the $367,000.

At this point, the return you get is much more important in terms of growing your portfolio.

Step #4: Invest, reinvest and eventually retire

The importance of getting a high return is that it can save you literally years of working, so then you can retire faster. For most people, if you're starting with $30,000, save $2,000, 8%, then it will take you around eight years and you'll just be comfortable living your current lifestyle.