Capital gain taxes in Canada can be confusing.

Typically, you are taught that capital gain tax is around 25%, but what does that mean?

Does your capital gain tax change if you make a high income instead of a low income?

If you can choose between invest and get capital gain versus work and get employment income, which one should you should to maximize your after tax income?

Here’s an interesting quote that I want to share with you:

I just thought it was pretty funny, but I do believe that you should pay taxes if you are obligated to. However, if there are ways where you can reduce your taxes legally, then by all means you should do that as well.

Investment Taxes

When it comes to investing, one of the things you cannot avoid and overlook is taxes. No matter where you reside - Canada, US, Australia, you are required to pay capital gain taxes.

In this Investment Taxes series, I am going to show you how to calculate Capital Gain Taxes in Canada, and in the US.

Then, we will go through some scenarios illustrating the comparison between investing and working, and high-income vs. low-income earnings.

Introduction to Taxes

The goal of this series is to educate you in taxes and help you save thousands to hundreds of thousands of dollars in taxes.

Overall, the long-term benefits of taxes are very important and you can imagine them as the “rule of the game”. If you can understand the rules very well, then you will be able to use them to your advantage.

In today’s blog post, I will show you how to calculate Capital Gains Taxes for a Canadian citizen. If you are a US citizen, make sure to tune in to my next blog post where I will show you how to calculate Capital Gains Taxes in the US.

Capital Gain or Loss - Official Definition

Capital Gain or Loss, as described by the CRA website, is when you sell or are considered to have sold capital property.

Capital property can be a physical property like real estate, or it can be a share which is a piece of paper in theory.

According to the CRA, any of the following actions will also be considered selling or disposing of your property. For example, when you exchange a property, you transfer a property into a trust and you give the property to your grandkids as a gift (which I do not recommend doing by the way).

Some other examples of “sold property” are converting some of your shares, settling a debt, or if the owner of the property dies, or leaves Canada.

If you would like to see more scenarios, you can check the CRA website for a more comprehensive list.

The official definition of a Capital Gain or Loss, is that 50% of Capital gains are taxable - but what does that really mean?

Capital Gain or Loss - Example

Here’s an example to help you understand.

Let’s say you’re investing $100,000 into the stock market and you made a 30% return (which is our % return goal). This means you then have a $30,000 gain, and let’s pretend you exited all of them at the end of the year in December.

You now have $30,000 worth of gains, and 50% of that is taxable, so you include $15,000 on your tax return … but at what rate will you be taxed?

To answer this question, I will elaborate the two main scenarios that are applicable to this situation.

For the first scenario, you are a high-income earner - a full-time professional earning over $150,000 per year who is in the highest tax bracket.

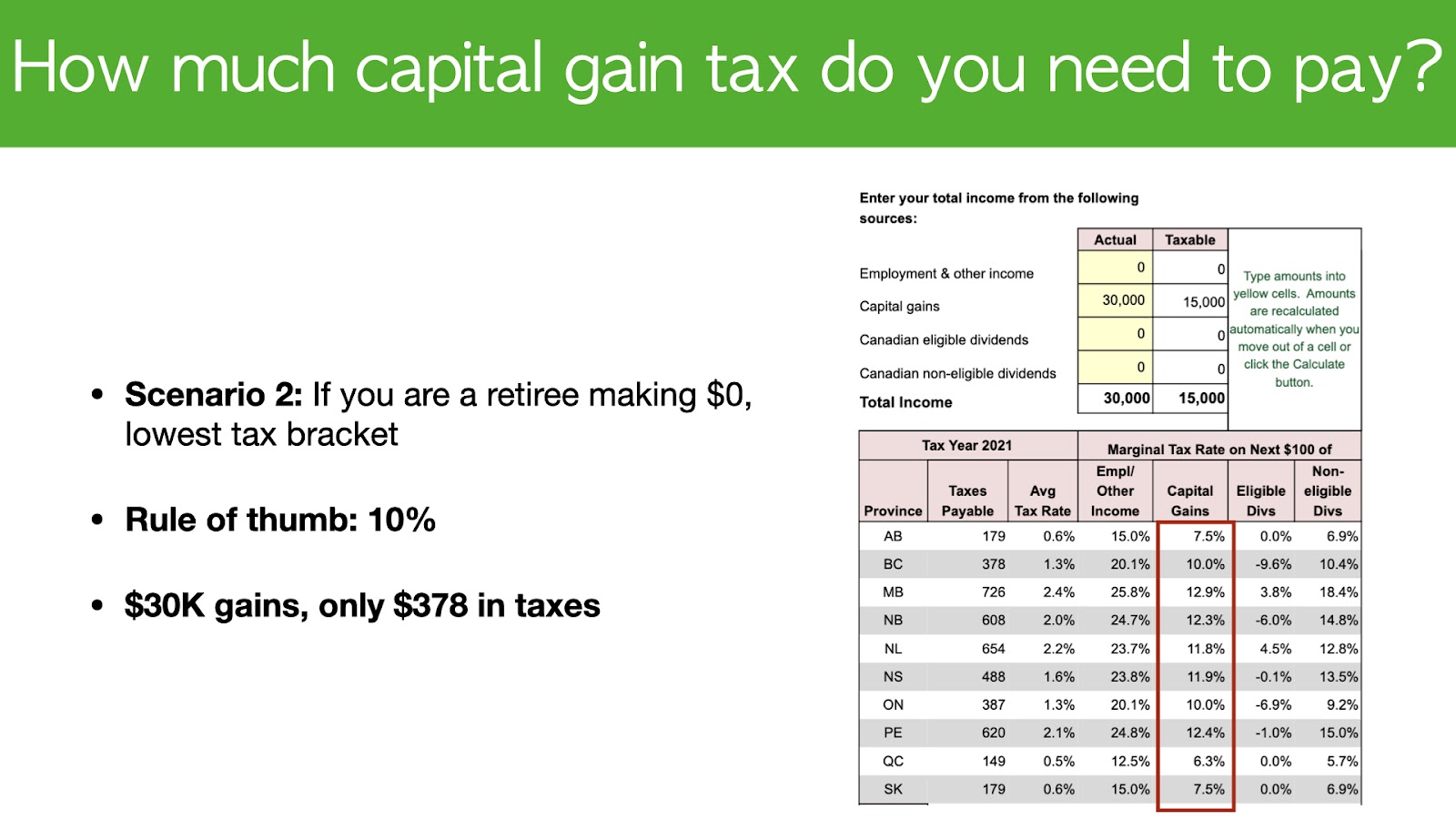

In the second scenario, you are a retiree making $0, in the lowest tax bracket and for some odd reason, you do not have pension.

For the following scenarios, here is one of my most useful tools I found online to calculate taxes, provided by:

https://www.taxtips.ca/calculators/basic/basic-tax-calculatr.htm

Scenario 1 - High Tax Bracket, High Income Earner

In this scenario, you are a full-time professional earning over $150,000 per year and you are in the highest tax bracket in Canada. The rule of thumb for those in the highest tax bracket is 25%, which means that 25% of your earnings will be taxed.

In our previous example, if you have earned $30,000 in Capital Gains then you are paying $15,000 in tax, which is 50%. Following our rule of thumb, 25% of the $15,000 rounds up to be ~ $4,000 worth of taxes included as capital gain.

To give you a visual representation, here is a screenshot from Tax Tips Calculator:

If you take a look you will see that any additional capital gain earnings will be taxed at approximately 25%.

If you live in BC, you will be paying $46,000 worth of taxes. If you use the calculator and exclude this $30,000 of capital gain, then you will be paying $42,000 of income taxes (which is capital gain related tax), with the incremental part adding to ~$4,000.

So what does that mean?

With $4,000 you can get 2000 donuts from Tim Horton’s, four Playstation 5’s, or even 2 months of rent depending on what kind of condo you’re renting. So $4,000 can be quite significant - it can definitely replace a lot of meals, so that is why it’s so important to be aware of how much taxes you are paying.

Scenario 1.5 - Working but not Investing (Alternative)

So what if you decide not to invest $100,000 with 30% return, and instead you work very hard, working overtime hours and you earn an extra $30,000. How would that impact your tax return?

In our scenario, instead of $150,000 of employment income, you now have $180,000 of employment income.

Here is a revision of our taxes, with $180,000 and 0 Capital gain. In BC, your taxes payable is now $54,000.

Even though I am getting the same amount of output before tax which is $180,000, I am being taxed more because I work more. This means that I am paying $8,000 in additional taxes, and my taxes have increased from $46,000 (From working & investing) to $54,000 (Working overtime & no investments).

Therefore, there are huge benefits to investing that $100,000 and making a 30% return even if you have to pay some taxes (around 25%). You are still better off and will have more money in your pocket after you’ve paid the government.

This is called working smart instead of working hard.

Scenario 2 - Low income or retired (earning $0)

This is an extreme example, because I assume you have no pension, no old age security, and you’re at the lowest of low in terms of tax brackets.

The rule of thumb for the lowest tax bracket, is 10%.

Here is a chart for the lowest tax bracket.

If you have a capital gain of $30,000 and only half of that is taxable, then you have $15,000. If you take a look at BC, you will find that Capital Gain is approximately 10%, and this percentage varies slightly with provinces.

For your own individual calculation, you can refer to the province you are living in.

In this case, taxes payable amounts to only $378 which is significantly less than a high-income earner in a higher tax bracket.

That means you have high incentives to make a capital gain when you are making a low income, because with $30,000 of gain, you are only paying ~1% in capital gains tax, which is $378.

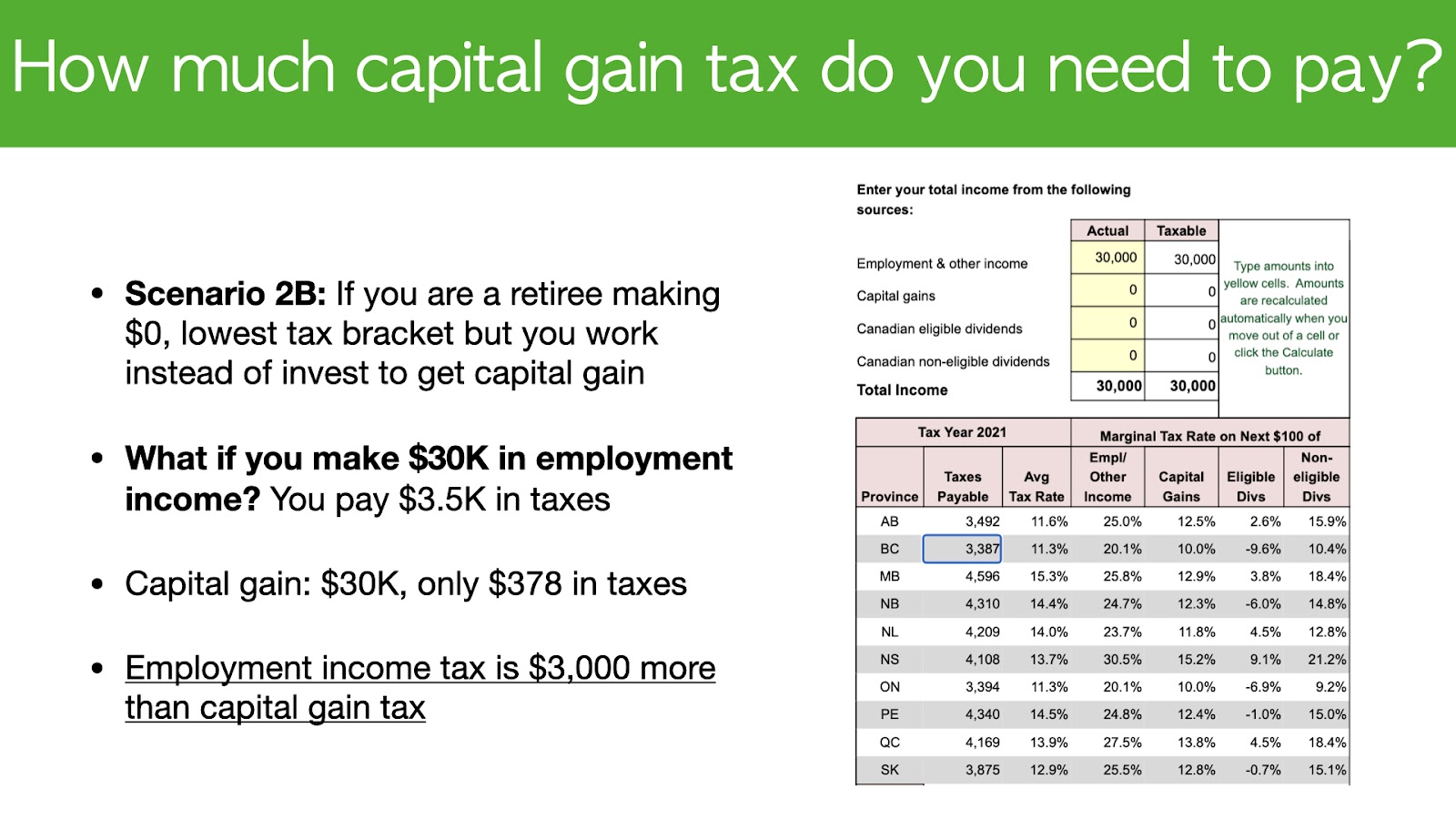

Scenario 2.5 - Retiree (Alternative)

In this alternative situation, let’s say you are a retiree with a part-time job.

You are earning $0, but instead of capital gain, you have a part-time job. You then have an employment income of $30,000, and you start from the lowest tax bracket.

In this case, all of your earnings of $30,000 (or below) are entirely taxable in BC.

Here, the taxes payable is $3,387. If you refer to our example above for $30,000 in capital gains earnings (taxes payable $378), you are actually paying about ~ $3,000 more in taxes with your part-time job.

In this scenario, it is much better for you to invest $30,000 in order to save the $3,000 in taxes you would have to pay if you were working a part-time job.

It’s a bit counter-intuitive when you think about it, and it all depends on the source of income you’re getting. In other words, if you are working instead of investing, you’re actually losing money every year.

So welcome back to my channel. And in this video series, we're going to talk about investment taxes. Now, when it comes to investing, one of the things you cannot avoid and overlook is taxes. No matter whether you're in Canada, us Australia, you need to pay capital gain taxes. So in this video, we're going to talk about how to calculate capital gain taxes. And we're going to do a couple of comparisons between investing versus working, whether you're a high income earner or a low income earner, like a retired person. So let's get started.

Series is really to help you to save a thousand dollars, $10,000 or even a hundred thousand dollars in taxes. So the overall long-term benefits of taxes is quite important. And you can imagine taxes like the rule of the game. And if you understand the rules very well, then you can use it to your advantage. So in this investment tax series, I have prepared 11 videos so far, and this is the fair first one. So in this video, we're going to talk about calculating capital gain tax. If you're Canadian and in the next video, we're going to calculate capital gains tax. If you are a us citizen. So it's a bit different and we're going to break that into two different videos and you can look at this slide and you can see the upcoming videos that I have planned for you. Now, moving along, I just want to celebrate another success story within investing a celebrator where Chris made 53.6% from saver.

So that is fantastic return. Congratulations, Chris, I'm glad you mastered investing and now you're getting phenomenal return. Looking forward to your next one. Now, in terms of subscribers, I know 98.2% of you guys are not subscribed yet. So it will really help me out if you just click the subscribe button and it notification bell, and it is free and you can always change it in the future. So right now I'm doing a a hundred likes giveaway where I'm giving a way the book, rich dad, poor dad by Robert Kiyosaki. So here it's actually one of my favorite investing slash personal finance books that I read when I was younger. As you can see, there are a ton of reviews on Amazon. And if you'd like to get this book, then hit like, and leave a comment below. And once we reach a hundred likes, I'll select a winner down below.

Now, what is capital gain or loss? Now capital gain from the CRA website is really when you have sold capital property. Now this can be a physical property like real estate, or it can be a share, which is a piece of paper in theory. Now, if you do any one of these things as well, you will also be considered as being disposed of, or have sold that property. For example, you exchange a property, you transfer a property into a trust and you give the property to your grandkids as a gift. And that is a big no-no don't do that. Um, and you convert some of your shares. You settle a debt like as you can see, the list goes on, like for example, leaving Canada that is treated as you have sold the property, even though you actually still have it, or somebody dies, uh, the property will be sold at that time as well.

So, yeah, so that's how capital gain and loss are triggered. Now the official definition is that 50% of the capital gains are a taxable, but what does that really mean? So let's say you're investing a hundred thousand dollars in the stock market and you made 30% return, which is the goal we aim for. So then you have $30,000 gain, and let's say you exited all of them, you know, at the end of the year, which is December 31st. So that means you have $30,000 worth of gains. And 50% of that is taxable, but at what rate, and that's the question that we'll be answering shortly. So let's say 50% of that is taxable. So you include 15 K on your tax return. Okay. Now there are two main scenarios when we're talking about this. The first scenario is if you are making a lot of money, like if you are a full-time professional making over 150 K a year, we'll do a scenario on that because you'll be in the highest tax bracket.

But if you are also a retiree and you're making $0 and you're at the lowest tax bracket, because for some odd reason, you don't have pension. We'll look at that as well. Now, one of the useful tools I found online is a tax calculator provided by tax tips.ca. Uh, so I'll include the link below in the comments section. So you can check that out, but basically I've played around with a couple of scenarios. So then it will help you better understand what is the amount of taxes you need to pay. If you make 30%, which is $30,000 of capital gain this year. Okay. So scenario one, you are a full-time professional making over 150 K a year. This means you're a tax at the highest bracket in Canada. So the rule of thumb is really around 25% of the game will be taxed. So for example, with 30 K gain, you pay 15 KT tax, which is 50% at eight times 25.

And then so is around 4k of taxes that will be included as capital gain. So with 30 K gain, 15 K is taxable. And if you take that and times it by 25%, then it's approximately $4,000 worth of taxes. So on the right-hand side, this is actually a screenshot from tax tips calculator. And here you will see that as you make any additional capital gain or be taxed at approximately 25% or so. And for BC in total, you'll be paying $46,000 worth of taxes. If you actually use the calculator and you exclude this 30 K of capital gain, then you will be paying 42 K of income taxes. So that means to capital gain related tax. The incremental part is around $4,000 or so. So what does that really mean? I mean, with $4,000, you can get 2000 donuts from Tim Horton's. You can get four PlayStation size and you can even pay two months of rent depending on what kind of condo you're renting.

So it can be quite significant. It can definitely replace a lot of meals. So that's why it's so important to be aware of how much taxes you're paying now. What if you don't invest instead of investing a hundred K and getting 30% return, you just work, you work over and you earn an extra 30 K. Now, how would that impact your tax return? So instead of 150 K of employment income, right, you have 180 okay. Of employment income. So here on the right hand side, you'll see that my screenshot is actually revised now and is 180 K and I have zero capital gain. And if I go back here and look at the BC line, which is the second line, British Columbia, my taxes payable is actually $54,000. So even though I'm getting the same output before tax, which is 180,000, but because I work more, I actually get taxed more.

So I'm actually paying $8,000 in additional taxes. So my tax increased from 46 K, which is BC, which has a mix of capital gain and employment income to 54 K if I'm just working overtime and I don't invest at all. So when you think about it, wow, there is actually a benefit to investing that 100 K make 30% so that even though you're paying some taxes, which is around 25% are still better off, you have more money in your pocket after you've paid a government. And that's okay. What's really matter because now you're working smart instead of working hard, uh, imagined you saved yourself, you know, $30,000 worth of gold. Okay? So by working more to earn that extra 30 K of employment income, you're actually losing 4,000 donuts, uh, because nowadays nobody measures anything in metric anymore. We measure things in doughnut, in Canada.

All right. So let's talk about scenario two, if you are retired and he makes $0, and this is an extreme example, because I assume you have no pension, no old age security. And you're at the lowest of the low in terms of tax brackets. And here, you'll see that's on the right-hand side. I have the screenshot here and a capital gain is $30,000, right? And only half of that is taxable. So 15,000. And then afterwards, if you look at DC, then you can see the capital gain is approximately 10%. And you can see a difference by provinces, but you can just look at the problems that you're living in and refer to that. So in terms of taxes, payable is only $378. So that's a lot less. So that means you have a lot of incentive to make a capital gain when you are making a low income, because with $30,000 of gain, you're only paying 1% in capital gains in taxes, which is $378.

So I'm not going to do the donut calculation in this case, but let's look at an alternative situation and let's say, you're a retiree and you got a part-time job. So you're making $0, but instead of capital gain, you get the tar time job. So then you have employment income of $30,000. So you'll still start from the lowest bracket. And then you start calculating up from there. And here, you'll see that on the right-hand side, the screenshots $30,000, all of 30,000 is taxable and below. You'll see that for BC, the taxes payable is $3,387. So when you do that comparison, it's actually 3.3 here. Um, for capital gain is 30 K, which is three, seven, eight in taxes. And now because you're working your get a part-time job, you actually pay $3,000 more in taxes. So in this scenario, it's much better for you to invest 30 K to save that three K in taxes instead of working it's a bit counter-intuitive, isn't it, it's all because of the source of income you're getting, imagine you are working for a company for free, and then the share price goes up.

So then you sell the share and you get that gain instead of getting an employment income. That's interesting, isn't it? So by working, instead of investing, you're actually losing 1500 doughnuts a year, and that's, that's crazy. That's a very high amounts of donuts. Like if you divide that by 365 days, that's a couple of donuts a day, that's enough to feed a grown man everyday for, you know, Tim Horton donuts for the rest of their lives, uh, for that year. So in a future video, I'll teach you how to save 2000 donuts a year, which is approximately $4,000 in terms of taxes when you invest a hundred K in the market. So that's around five donuts a day. Uh, so that's definitely gonna make a huge difference in your life. And there's an interesting quote that I want to share with you, you know, collecting taxes that is absolutely necessary is legalized robbery.

Yeah. I just think is pretty funny. Uh, but I do believe that you should pay taxes if you are obligated to, but if there are ways where you can reduce your taxes legally, then by all means you should do that as well. So just want to share my vision for myself of you. And my goal is really to make around 30% return a year. And when I first started, that seemed like a stretch goal to me. You know, when I first started, I was actually losing money when it comes to investing, I had a lot of ideas. I have a lot of strategies, but none of them work. So then I had to test out and figure out which strategy work, which strategy doesn't. And that took eight years of time. And after I mastered investing, I have a very simple, profitable and straightforward strategy.

And I focus on buying stocks that are on a discount and then multiply my profits, using something called stock options. And that's when I also created a coaching program called investing a celebrator. So here you will see Chris case study. He's the 63rd case study where he made 53.6% from Sabre in just under one month. So that's a phenomenal return. And of course we always focus on long-term investing, but when the market gives us more profits, then we're happy to take it as well. So in terms of the next steps, if you really want to learn more about investing and how to get a high return, then I would suggest you to click the link in the description, call it a free case, study, how to get 30% from the stock market in the next 12 flats. It should be the first link down there, and you can watch the four hour webinar.

It's insane. It's extremely long. Uh, if you're a full-time professional, then you probably need a cup or two cups of coffee before you start, because I've packed a ton of value in that video. So in the next video, we're going to talk about calculating capital gain tax for USA. And if you are living in us, then this video is made for you. And in a future video, we're going to talk about capital gains strategy, investing, tax strategies to help you reduce capital gain tax. So when you're investing your first 100 K, you should pay zero, zero in taxes. So make sure you watch that video and yeah, happy to connect

[inaudible].