Today, we’re going to dive into capital gain taxes in the US. When you’re investing, it is crucial to know how much capital gain taxes you need to pay and whether it is worth it or not.

We will be going through short-term capital gains, long-term capital gains, and a few different scenarios based on the amount of income you’re making and how much capital gains taxes you will have to pay.

The goal of this series is to help you save a thousand or tens, or hundreds of thousands of dollars in taxes. Previously, I wrote a post on Capital Gain Taxes for Canada, so if you are a Canadian citizen you should check it out.

In the future, I am also going to give a few tax-planning strategies to help you make better informed decisions, whether you want to become a day-trader or a long-term investor, or you simply just want to save on taxes completely. Stay tuned!

Short-term Capital Gains

There are two types of capital gain tax in the USA, short-term and long-term. Short-term is very simple and is basically like day trading, when you hold onto investments for less than one year.

When you hold onto your investment for less than one year, then it is taxed in the same way as your regular income.

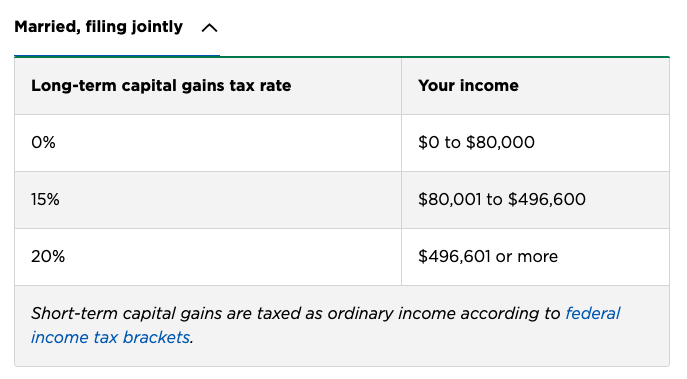

However, if you end up holding onto the investments for more than one year, then you get 3 different tax rates: 0%, 15%, and 20% depending on how much income you made and which state you’re from. There are also two levels of taxes, one in which you pay to the federal government, and one in which you pay to the state.

I went online and found a tax calculator called SmartAsset.com , which you can use to calculate your taxes as well.

If you live in California where the state taxes is 14.3%, that is actually quite high and when you combine it with federal taxes, your taxes can be somewhere between 25-30%.

The next in line is Hawaii, Oregon, and Minnesota.

The states with least taxes include Texas, Florida, and Alaska to name a few, and if you’re looking to save on your capital gain taxes, then you might consider moving to one of these states.

Scenario 1: High-Income Earner

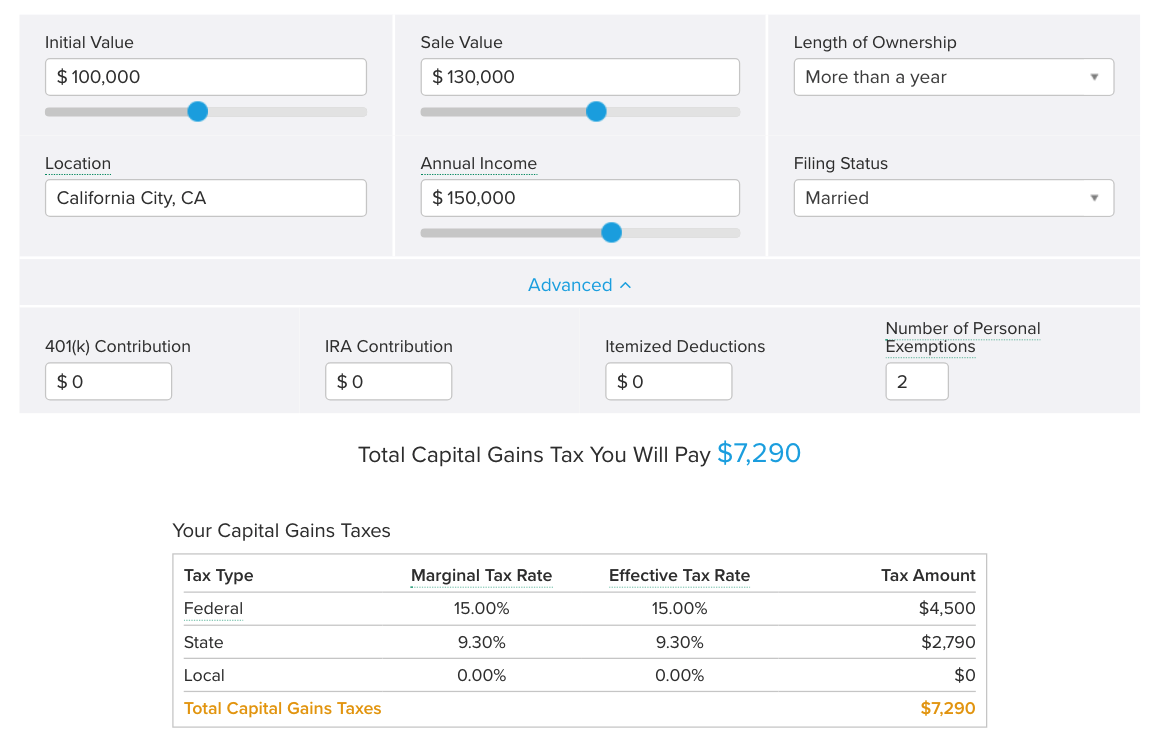

For the first scenario, let’s say that you are a full-time professional making over $150k per year with some sort of a tech job. This means that you’re almost at the highest tax-bracket.

Using the calculator from SmartAsset.com, here you will see that I entered $150,000 for new income, with a capital gain of $30,000 with more than 1 year of ownership - and I live in California.

This means that I will be taxed for $4,500 at the federal level, and $2,790 at the state level. Together that’s around 25% and when it comes to capital gain taxes, you will be paying $7,290.

Alternative Scenario:

If you choose not to invest and instead, work harder overtime and earn $180,000 instead of $150,000, then in this case you will be paying only income tax for your employment income.

Here is the calculation for it:

With investing, you pay $45K in taxes and if you do not invest at all, you will be paying $47K. That means by working harder to earn that $30K, you actually pay an additional $2K in taxes.

That means you have less money in your pocket at the end of the day, despite working harder. Isn’t that a bit counter-intuitive? That $2000 could have been used to buy hundreds of cheeseburgers, a PlayStation 5, or pay for a month’s rent.

By investing and getting a 30% return and paying less taxes, you actually save yourself a ton of work and money. Let’s move on to the next scenario.

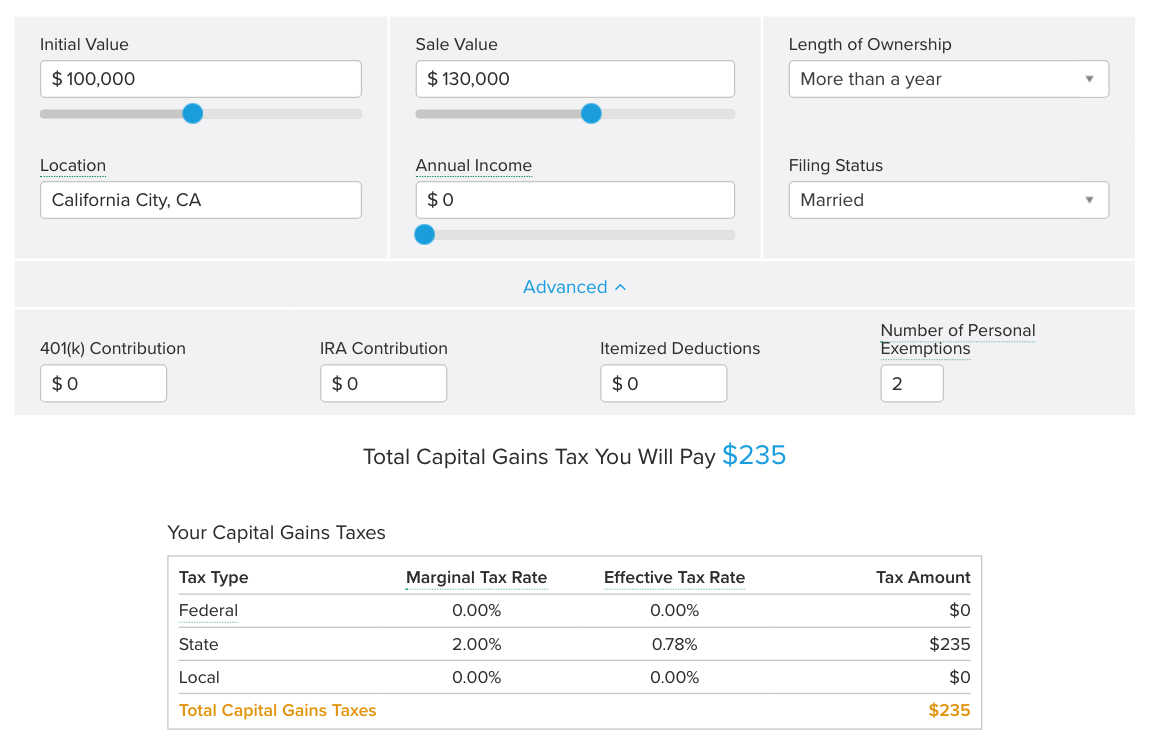

Scenario 2: No-income Earner

Let’s pretend you are making $0, you are in the lowest tax bracket, and you earn $30K in capital gains. In this case, you will be paying $235 in taxes.

In this calculation if you don’t invest and instead work to earn $30K, you will be paying $3097 in taxes. Comparing that to capital gain taxes of $235, you’re actually getting taxed a lot more for working - In a way, you’re being penalized for being employed because you’re paying employment income tax, payroll taxes, and so forth.

In that way, it’s better to invest $100K and make a 30% return than to work harder to earn $30K. Of course there is going to be a balance between the amount of income you make versus the amount of capital gain you make but you can always choose between the two on any given day, and I would suggest that you choose capital gain because this leaves you with more money in your pocket.

Mind Your Taxes

To wrap up, here is a quote from Winston Churchill about taxes that I found very interesting since we are now in a post-pandemic period.

This means that there was a lot of money printing, a lot of money handed out in stimulus checks and other means, and as a result we will have future consequences in the following years in which there will be higher taxes to repay for money printing and loans.

So the question is - Do increased taxes really increase prosperity in the country? Do they actually speed up economic activity in the country?

This is going to be such an important decision and topic.

I won’t be able to cover it in this blog post, but by showing you how capital gain versus employment income are being taxed, I hope you can start to understand how the government is trying to incentivize you.

Now imagine you are a person that doesn’t know how taxes work. If you are a person that is just trying to work hard and be a good American citizen, are you really maximizing the amount of money in your pocket?

At the end of the day, are you taking the most money back home? This is why educating yourself on taxes is so important.

So in this video, we're going to talk about capital gain taxes in the United States. So when you're investing, it is very important to know how much capital gain do you need to pay and whether it is worth it or not. So that's what we're going to dive into, you know, do you know what a short term capital gain do, you know, what's long-term capital gain and what are the different scenarios based on the amount of income you're making and how much capital gain taxes do you have to pay? So let's get started. So how much capital gain tax do you pay for stocks in the United States? The goal of this series is really to help you save a thousand or 10,000 or even a hundred thousand dollars in taxes. And this is the second video when it comes to investing tax and previously we covered the Canadian side.

So now we're going to cover the us side in the future. I'm also going to cover a couple of tax planning strategies to help you make better decisions, whether you want to become a day trader a long-term investor, or you want to save on taxes completely. Now, before we start, I just want to celebrate another success story from Allen, where he made a 90% gain from FedEx and Brad also make 58% from SPC and 41% from Lou lemon in four months. So one of my favorite things about this case study is that Brad was actually telling his wife that he was going to buy Amazon, but the wife thought he wants her to shop on Amazon. So then she went on shopping instead. So you can pause this video and read this case study. So now in terms of the a hundred likes giveaway campaign for this video, the book is rich dad, poor dad.

So if you haven't read this book before then I would definitely recommend it because it really changes your mindsets in terms of being an employee, being an investor, being a business owner and being self-employed. So it's one of my favorite personal finance books. And if you leave a comment below click like on this video, and once we reach a hundred likes, I'll select a winner to get a copy of this book for free. So make sure you gently tap the like button on this video. So let's get started. Now, let's start by looking at capital gain tax and there are two types of capital gain tax in USA. One is short-term and one is long-term and it's very, very simple for the short term tax. It's basically like day trading, short term trading as when you hold on to the investments for less than one year.

And if you hold onto the investment for less than one year, then it is taxed the same way as your regular income. Now, if you end up holding onto the investments for more than one year, and then you get three different tax rates, which is 0%, 15% and 20%, depending on how much income you make. So I went online and I found a tax calculator called smart asset.com. So here it is. And I did a couple of scenarios. If you're living in California, based on how much income you make, how much taxes would you be paying now, when it comes to capital gain tax, we're going to focus on long-term capital gain tax in this video. And there are two levels. One is where you pay to the federal government. And one is where you pay to the state. And for federal, like I mentioned earlier is zero 15 and 20%, depending on how much money you're making and state.

It depends on the state and the highest capital gain taxes, California, where to state taxes is 14.3%. So that's actually quite high. And when you combine it, your taxes can somewhere between 25 to 30 something percent. And for the next highest as Hawaii, Oregon and Minnesota, and the lowest States are, uh, listed here. For example, Texas, for example, Florida, for example, Alaska. So if you want to save on your capital gain taxes, then you might consider moving to one of these States. Okay? So in terms of the scenarios that we will go through first, I'm going to assume you are a full-time professional making over 150 K a year, probably some sort of tech job. And this means you're almost at the highest tax bracket. The second same arrow is that if you're a retired person and you're making $0, and this is the most extreme scenario and you were at the lowest tax bracket.

So first let's look at the professional one. Now, if you're a professional making 150 K a year and means you're almost at the highest tax bracket, but not yet. So here you will see that I entered $150,000 for any new income. And then afterwards there is a capital gain of $30,000. And I selected more than one year for length of ownership and you're living in California. So that means you'll get taxed for the 500 at the federal level and 2,790 at the state level. So together it's around 25%. When it comes to capital gain tax, then you'll be paying $7,290. Okay. Now what if you don't invest? What if you just work harder, you get some overtime and instead of 150 K you make 180 K. Now in that case, you will be paying just purely income tax, your employment income. And here is the calculation for it.

With investing, you pay 45 K in taxes, which I've showed you earlier. And if you work and not invest at all, you'll pay 47 K. So that means by working harder to earn that 30 K you actually pay two K more in taxes. And that means you have less money in your pockets at the end of the day, when you work harder, that's a bit counter-intuitive, isn't it. And that means you can use that $2,000 to buy cheeseburgers. If you want to buy a PlayStation five, if you want to, you can pay for a month's rent. If you want to, by investing and getting 30% and paying less taxes, you actually save yourself a ton of work and money as well. So now let's jump to the other scenario. What if you are making $0 at the lowest tax bracket and you make 30 K in capital gains.

Now in that case, you'll be paying $235 in taxes, and you can see it in calculation shown on it right now, if you don't invest and you work to make 30 K instead, you will be paying 3090 $7 in Texas. And when you compare that to capital gain of 235, you're actually getting taxed a lot more for working in a way you're being penalized for being employed, because you're paying pers employment, income tax, or paying payroll taxes, so on and so forth. So it's much better to invest a hundred K and make 30% then to work harder and make 30 K. Now, of course, there's going to be a balance between the amount of income you make and also versus the amount of capital gain you make. But if you can choose between the two on any given day, then you will choose capital gain because this gives you more money into pockets.

At the end of the day, in terms of cheeseburgers, that's 1400 cheeseburgers that you save by investing. That's three PlayStation fives. That is one and a half months of rent. So by working, instead of investing, when you're retired, you are really losing 14 cheeseburgers a year. And in the future video, I'll teach you how to save, you know, more cheeseburgers, how to save on more taxes when you invest a hundred thousand dollars in the market. And before we wrap up, I just want to finish with a quotes from Winston Churchill about taxes, can a people tax themselves into prosperity, can a man stand in a bucket and lift himself up by the handle? And this is very interesting because right now we're in the post pandemic period. And obviously there was a lot of money printing. There was a lot of money headed out through syrup and other means, and the consequences that's in the future years, there's going to be higher taxes to repay that's amount of money printing or loans, Gough government, so on and so forth.

And the question is, well, does increase taxes really increase the amounts of prosperity in the country and does increase taxes actually speed up economic activity in the country. And that's going to be such an important decision and topic. I wouldn't be able to cover in this video, but I think just by showing you how capital gain versus employment income are being taxed, you can start to understand how the government is trying to incentivize you. And now you can imagine if you are a person that don't know how taxes work, if you are a person that are just trying to work hard and be a good American citizen, are you really maximizing the amount of money in your pocket? And at the end of the day, are you taking the most money back home? And that's why taxes is so important. And when it comes to my vision for myself, my goal is really to make 30% return a year from the market.

I have gone through the journey from learning by myself for eight years, trying a ton of strategies that didn't work. And I was struggling losing money. I was losing board and $10,000 to mastering investing, spending only one to two hours a week and making 30% a year. And now I teach people how to invest in the market and the four weeks coaching program called investing accelerator. So these are really the case studies from investing accelerator, where Alan made 90% from FedEx, where Brad made 58% from SPCG and also 41% from Lou lemon in four months. So that is pretty amazing. And I have a lot more of these case studies to share with you in the future. So if you want to learn more, then you can click on the very, very first link below, which is the free bio thinner, how to get 30% from the market.

So if you click on that, then this will bring you to the registration page where you can attend a four hour webinar. This webinar is an absolute beast, insane in terms of the amount of content I've packed. Pruitt's so make sure you grab a cup of coffee before you start watching. And in the next video we're going to talk about who pays more taxes are dividend investors, paying more taxes, our growth investor, paying more taxes. And this is a crucial concept because when it comes to retirement planning, when it comes to retiring earlier, you want to have a clear understanding of what kind of income you're making, how much you're making and what is the after tax amount. And this is geared towards Canadian investors. So if you are a Canadian watching this video, by some chance, then this video is definitely for you, and you'll be surprised by the results. So I'll see you in the next one.