PROCRASTINATING IS EXPENSIVE...

If you are thinking about investing this year or the next, or even a couple years from now, STOP.

In today’s post, I will briefly walk you through why you should invest TODAY and the best time to invest is now.

The longer you delay investing, the more money it will cost you. Surprisingly, what people think the cost of delaying investing is not as significant of a figure than what it truly is.

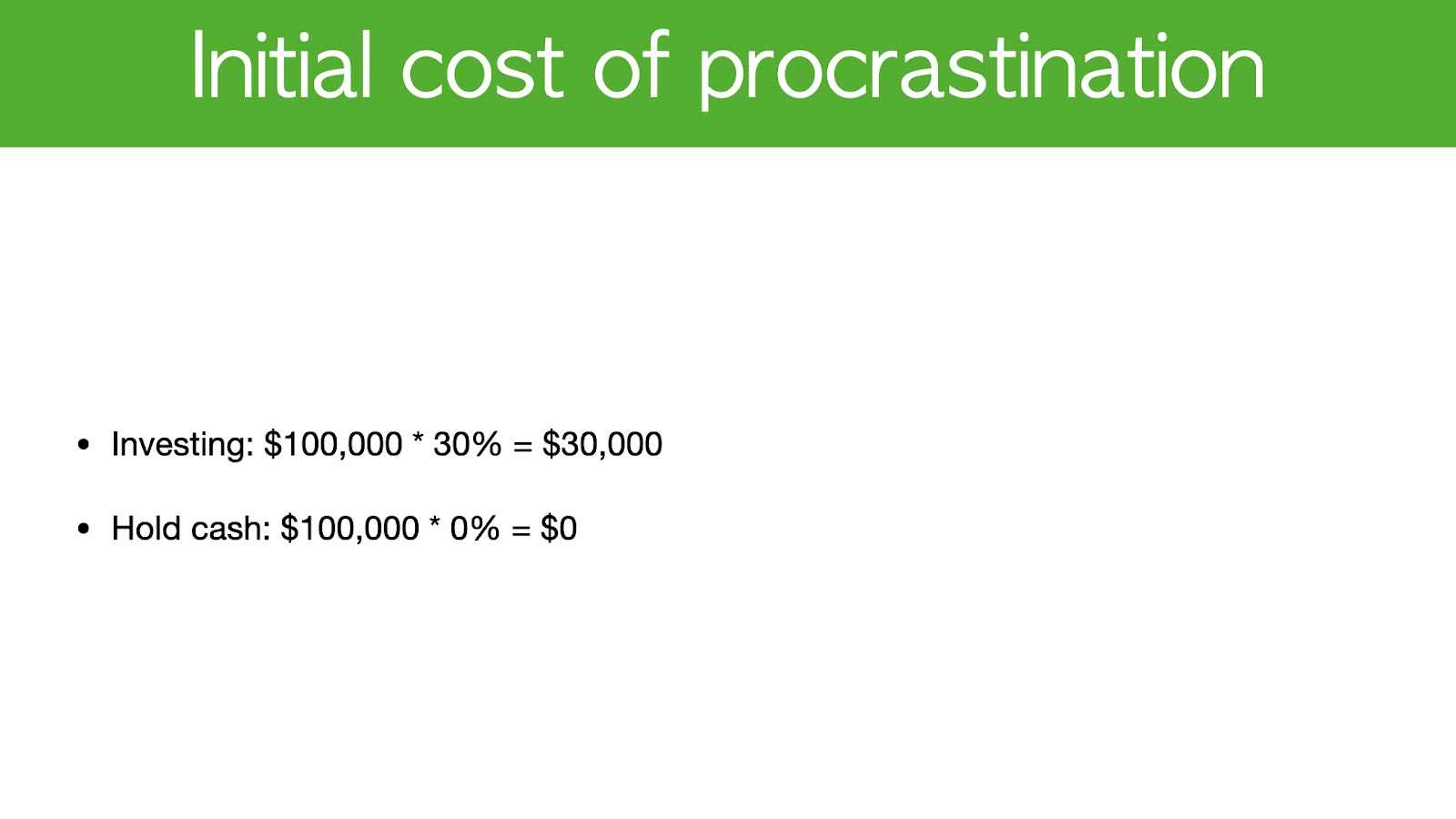

When people think about the cost of delaying investing, most people think that all they are missing out on is the gains for the first year.

For example, at the end of the day, S&P goes up by around 8% a year. If you invest $100K this year versus investing $100K in the next year, the difference is only 8%, right? So that’s only about $8,000 and it’s not really a big deal.

However, if you look at the bigger picture in investing, what the real cost of procrastination is, is that you lost gains for the last year.

Because next year, when you start investing again, you will still make that 8%.

You will still earn that $8,000 but as time goes on, the later you start costs you the last couple years of compounding.

Compounding is actually where you will experience the most growth, so your loss is actually more significant than you think.

Here is a calculation I’ve done to show you what delaying investing for 1 year looks like 10 years later if you invest $100K initially.

From the ninth year to the tenth, if you are making a 30% return your portfolio will go from $1,060,450 in year nine to $1,378,585 in year ten. So the difference for that 1 year is actually $318,000.

Therefore, when you are comparing yourself investing today versus yourself investing for five to ten years from now, what you’re missing out on is not really the initial years where you started investing, it is actually the last five to ten years you could have been compounding, and this is very important when you are closer to retirement, which is where you get the most gain.

If you study the curve of compound interest, you will realize the curve actually edges up higher and higher, kind of similar to the rates for COVID.

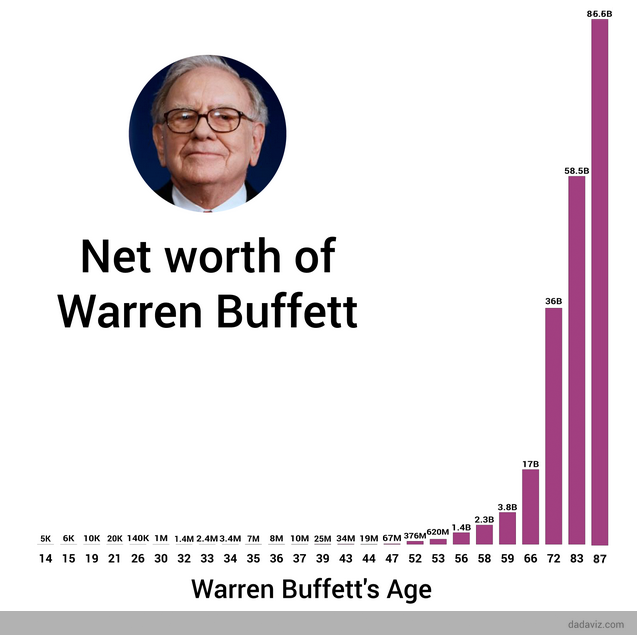

You want to capture that gain late in the years, and that’s actually how Warren Buffett earned a majority of his fortune.

You can actually see his fortune going up like a curve.

This is the reason I wanted to reiterate the urgency of investing and why I created this video.

If you are delaying investing , you are really losing out on the last couple of years of the compounding effect. In order to get a high balance when you retire, you need to start early.

NEXT POST…

So that is what I have to say on delaying investing and why I think you should not do it. In the next post, I will show you how to calculate return on investments for stocks like a real mutual fund.

This will be quite interesting because when I was doing research on the videos available on YouTube, I found that there were not very many videos available on how to calculate return on investment correctly.

I found videos giving simplified examples on how to calculate a one-year return, but none of them cover how to calculate your return when you are adding money, which is important because this is what really changes your return. So I will be showing you how to do it correctly, as well as how some brokers do it as well.

So you're thinking about investing this year or next year, or maybe even a couple years from now. And in this video, I'll briefly walk you through why you should invest today and why the best time to invest is this year and the longer you delay investing, the more money it will cost you. And surprisingly, what people think about the cost of investing is actually not the true cost of delaying investment. So before we start, I just want to say that 96.4% or you are not subscribed yet, and it is free. So you can always change your mind in the future and make sure you stay till the end for her to give away Andy winner announcement. So in terms of investing a celebrator, Mike has made another 42% from MSI in 3.5 months. So that is the 97 case study in the program. And this month I'm looking to help 20 professionals without a financial background to master investing and to target 30% a year.

The stretch goal is 30, and there'll be more details at the end of the video. People think about the costs of delaying investing. Most people think about what they're missing out is really the gains for the first year. You know, at the end of the day, S and P 500 goes up by around 8% a year. So if you invest a hundred thousand this year versus invest a hundred thousand next year, well, the difference is only 8%, right? So that's only $8,000. So it seems like it is not a big deal. If you look at the big picture and you really think about investing, what's really, the cost of procrastination is the last year. Because next year, when you start investing again, you will still make that 8%. You'll still make that 8,000, but as time goes on the later and later you start, what you're really missing out is the last couple of years off compounding.

And that's really where you experienced the most growth. So here, I've done a calculation that if you're investing with a hundred thousand dollars from the ninth to the 10th year, and you made 30%, your portfolio will go from 1 million and $60,000 to 1.37, $8,000. So 1.3 million. So the difference is Ashley $318,000. So when you're comparing yourself investing today versus yourself investing five, 10 years from now, what you're missing out is not really the initial years where you started compounding is actually the last five to 10 years where you want it to compound, and you're really close to retirement. And that's where you get the most gain. If you study the curve of compound interest, then you'll realize that the curve actually edges up higher and higher, kind of similar to COVID. You want to capture that gain really late in the years. And that's actually how Warren buffet made majority of his fortune.

He can actually see his fortune going up like a curve. So that's why I want it. You re iterate and create this video, because when you're thinking about the laying investing, it's really about the last couple of before you compound. And in order to get a high balance, when you retire, you need to start early. When it comes to investing, Michael for myself is really to make 30% a year. And when I first started, this seems like a stretch goal to me. I was actually losing money for eight years in a row, and my confidence was really low. And I don't have a proven and simple investing strategy. It took me eight years of trial and error to test 300 different strategies to figure out the strategy I'm using today. So after I mastered investing, my target now is to make around 30% a year.

And I have a very simple proven strategy that incorporates financial analysis, technical analysis news, so on and so forth. And I'm actually able to condense everything I know into a four week coaching program called investing accelerator. So if you want to learn about how I invest in the market, Danny can grab the four hour free training on my website, and this is perfect for you. If you're a full-time professional, you have no financial background and you want to manage your own portfolio with confidence. So to link his five minute investing.com/free case study, and it is the first link in the description. And after that program, Mike has made 42% from MSI in 3.5 months. So congratulations, Mike, this month, I'm looking to help 20 professionals without a financial background to master investing and target 30% a year. So to stretch goal is 30 people. So in terms of the giveaway, I'll be giving away Sam Walton made in America.

And it is one of the classic business books about how Walmart becomes so successful. So if we get a hundred likes, just tap like below and leave a comment and now select a winner in a couple of months. So from a previous video, I have selected a winner for the book harmonic trading too. So Dave, congratulations for winning this book. If you are watching this video, make sure you go back and send me your details and I'll send a book your way. So that is really it for this video. And in the next video, I'm going to talk about how to calculate return on investments for stocks like a real mutual fund. And this is quite interesting because when I was doing research on the videos available on YouTube, not a lot of videos cover how to calculate return on investment correctly. They usually give you a very simplified example, you know, how to calculate a one-year return or whatnot, but they don't really cover how to calculate your return when you're adding money, because that actually changes your return. If you're not doing this correctly, now some of the brokers will do it and I'll show you that as well. So I'll leave that to the next video.