DIVIDEND VS. GROWTH INVESTOR - WHO PAYS MORE TAXES?

So here’s the big question - Is it the Dividend Investor that focuses on getting a regular monthly - quarterly income? Or is it the Capital Gain Investor who focuses on momentum and hype stocks?

The answer to this question will impact how you plan for your retirement, and how you think about what kind of investor you want to be. At the end of the day, what you aim to be maximizing is the after-tax gain from your investments.

With this information, you can retire earlier and live a more comfortable and less stressful life. So let’s begin and talk about both Dividend and Capital Gain Growth Investors and find out which one pays more taxes.

This post is part of a larger series that informs you on how to calculate capital gain for the US and Canada. Here is a list of some of the other topics in the series:

If you are interested in some of those other topics, you can go back to some of my previous blog posts, and some will be released at a later date.

OVERVIEW

Today, we will examine several investing scenarios as well as the tax outcomes corresponding to each one.

Assume that you have a portfolio of $100,000 and you make either $30,000 in capital gain OR in dividend. In the first scenario we will examine earnings in the highest tax bracket.

In the second we will examine an average salary tax bracket, and the third scenario will be focused on a $0 income tax bracket.

We will be diving into what the taxes look like for each of these routes using a tax calculator you can find here:https://simpletax.ca/calculator

SOME CONCEPTS TO CONSIDER

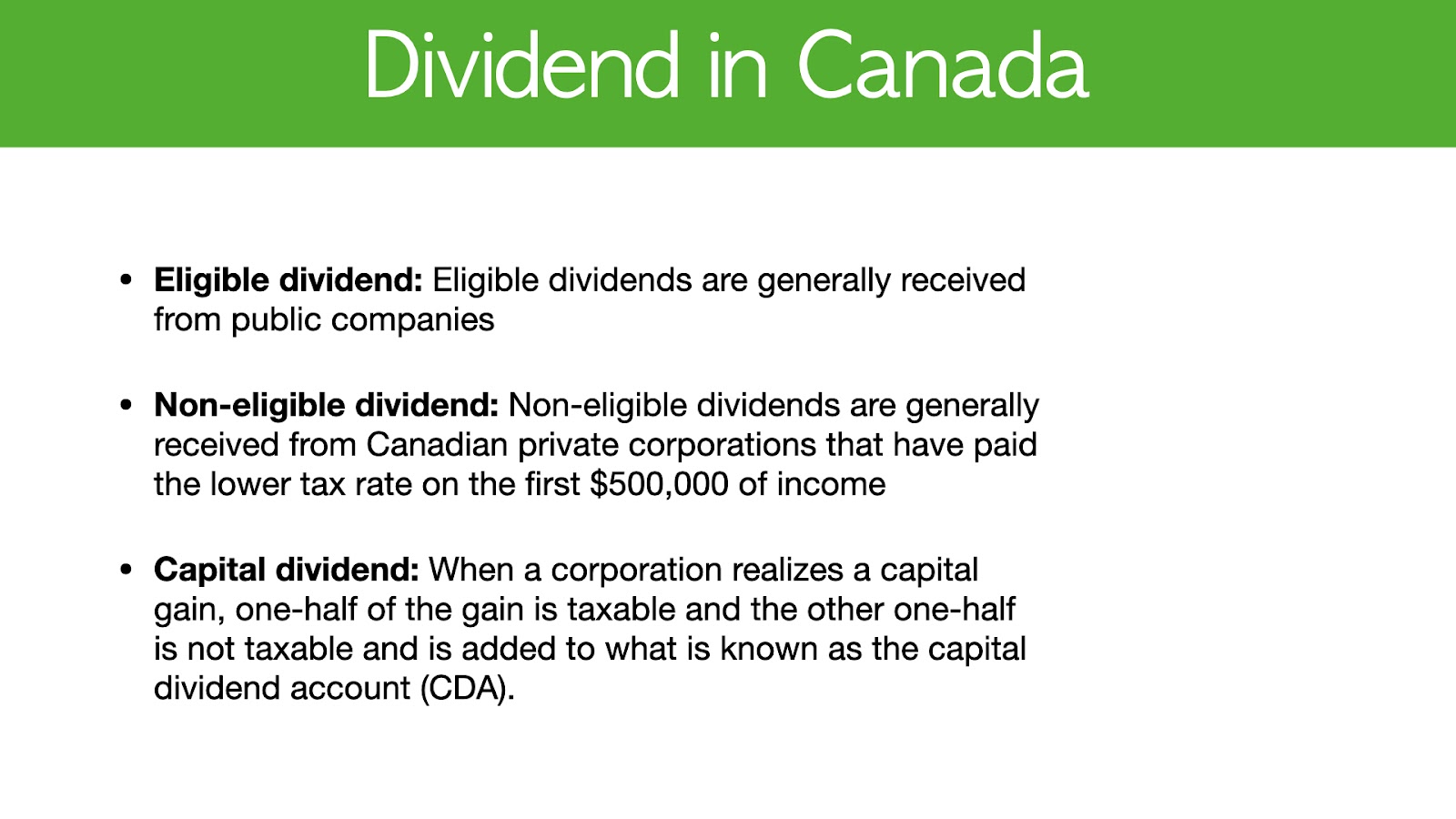

Before we explore each scenario, I first want to go through a few concepts on dividends, found from the CRA Tax Handbook.

If you invest in a stock from Toronto stock exchange, that is considered eligible.

Non-eligible dividends are generally received from Canadian private corporations to have paid lower tax rates on a first $500,000 of income.

Generally, this does not apply to you unless you have your own business. When you have your own business, your business profits will get taxed and you will be able to pay out a dividend to yourself, and this is why it has different rates than eligible dividends.

Lastly, Capital Dividend. When a corporation realizes a capital gain, one half of the capital gain is taxable and the other half is not taxable.

This is important because when you sell a property, you pay capital gain. If the corporation sells a property and then pays you in dividends, you do not get taxed on that dividend because the corporation already paid a capital gain.

This is a very important distinction. Most of the time, when you are getting dividends from public companies, the first one is going to be considered an eligible dividend.

Here are the tax rates in Canada. The reason that capital dividend is not taxed is because the corporation has already paid capital gains tax.

These are set rates and you will need to calculate your specific situation using a tax calculator. Let’s go through the scenarios.

SCENARIO 1

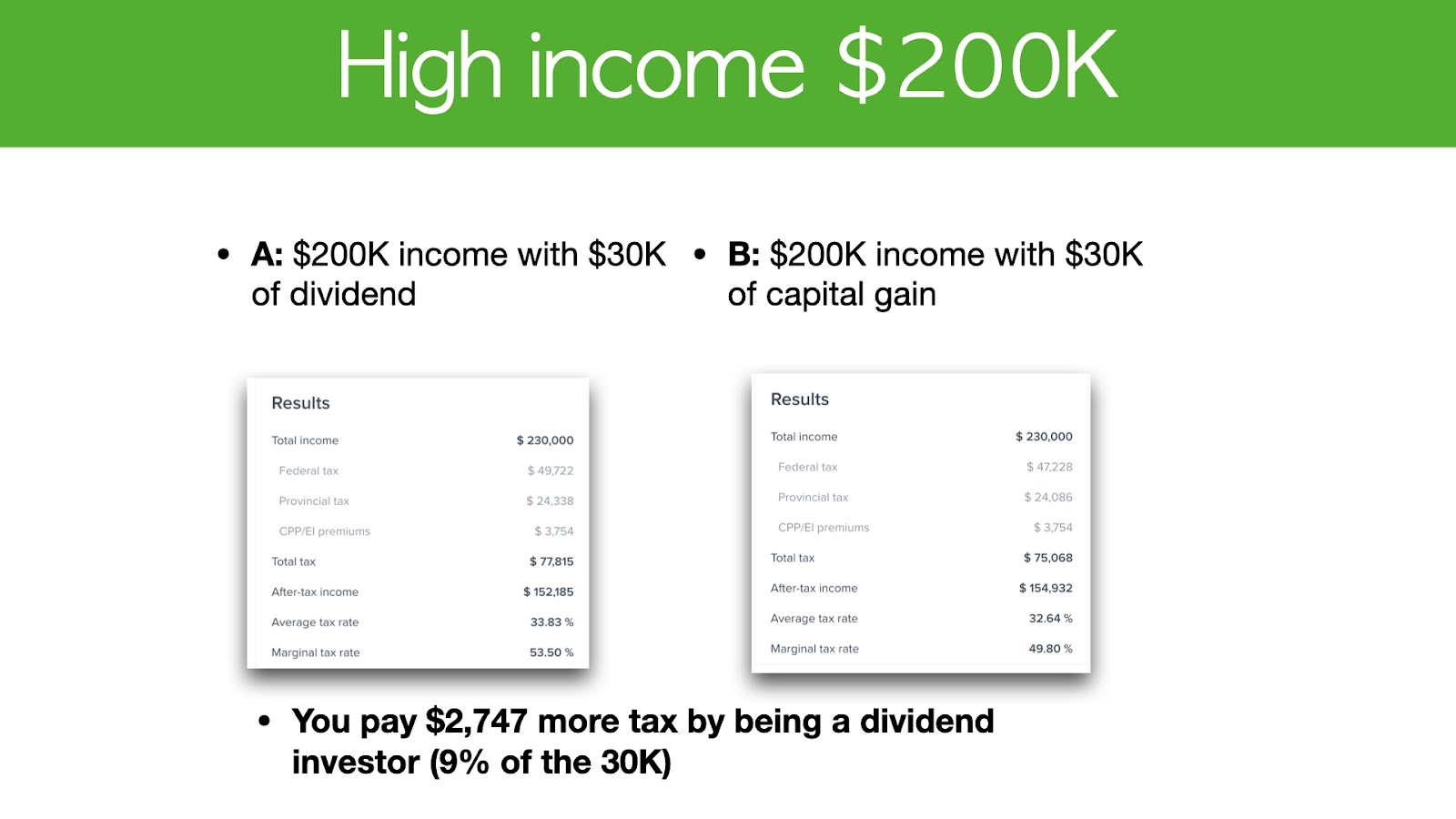

Your portfolio is $100,000, and you earn $200,000 per year putting you in the highest tax bracket and you earn $30,000 in capital gain or $30,000 in dividends (This could also be expressed in the format 30% capital gain or 30% in dividends, but because it is actually very rare to make 30% in dividend, we will express it as $30,000 for now).

So here is what it looks like if you are in the highest tax bracket:

On the left-hand side you have dividends and your total tax bill comes to $77,815.

On the right-hand side, your tax bill comes to $75,068.

In this interesting scenario, you actually pay more taxes by being a dividend investor. This is actually around 9%, which means that 9% of your total gain goes towards taxes.

When you are earning a high income, depending on which stage of the career you’re in, it’s actually disadvantageous to be a dividend investor, despite everyone telling you that this is the way to go because you’re getting a monthly income and so on, so forth.

The results here are that you end up paying more taxes, so you might want to rethink that strategy.

When you are making a high-income such that you are in the highest tax bracket, you should give some thought into whether you need money immediately, or whether you can wait.

This is a very important concept because if you don’t need money right now and you are reinvesting into the dividend, why bother paying the tax?

When you get dividend each year or on a monthly or quarterly basis and you reinvest it back into the company, that’s actually counterintuitive because you are paying more taxes and slowing your portfolio growth down as a result.

Therefore, if you are making a high-income and you are okay with leaving money in a stock for multiple years, then you should focus on capital gain.

The analysis I show here is actually just for one year, but ideally what you want to think about is the next 5 to 10 years because year after year if you are a dividend investor, you get taxed and taxed and taxed.

In contrast, as a capital gain investor you have the ability to keep compounding and you are only taxed at the very end when you exit, which is actually much more advantageous.

This is assuming you are not a day trader, you are earning a high-income, and you do not need the money immediately.

SCENARIO 2

For this scenario, you are earning a $70,000 income annually.

If you have $30,000 of dividend you pay $18,554 in taxes, and if you have $30,000 of capital gain you would pay $20,5000 in taxes.

In this case, you would pay about 6% (of $30,000 = $1,946) more as a capital gain growth investor than you would as a dividend investor. Why is this the case and why is it reversed from the previous scenario?

Let’s continue onto the third scenario, which will give you a better understanding of what’s happening.

SCENARIO 3

Imagine you are retired and don’t have any pension. You do not have any income and you only get $30,000 of dividend OR $30,000 of capital gain.

In this case you would pay $0 in taxes for $30,000 in dividend, and for capital gain you would pay $471 in taxes. In this way, it is better to be a dividend investor when you have less income.

When you think about this third scenario, it’s important to ask yourself when you will need the money because capital gain can also be considered paper gain.

This means that you don’t actually get the cash and that it is locked into shares, and the share price goes up. For dividends however, it actually gets paid out and becomes cash in your portfolio.

When you want to cash out and spend that money on something, you won’t have to sell any shares, and the number of shares you still have remains the same.

PLAN YOUR INVESTMENT

When you are trying to be a dividend or capital based investor, consider where you are in life and plan accordingly. Are you trying to take money out of your portfolio or are you trying to grow your portfolio to a million dollars? That distinction should be the main factor that sways your decision. Now to answer the question posed in Scenario 2, why does a capital gain investor pay more taxes than a dividend investor when you are in this particular tax bracket? In Canada, there is a concept called Marginal Tax Rates in which your tax rates are dependent on how much money you earn.

FEDERAL MARGINAL TAX RATE

On the right side of this table, you’ll see that in terms of federal taxes, your first $49,000 will be taxed at 0% for eligible dividends, while there is a 7.5% tax for your first $49,000 in capital gain.

This is only counting for federal taxes, and remember that our rule of thumb for capital gain is actually around 25%, including provincial taxes as well.

Following this logic, initially you would pay more capital gain tax (up to $89,000) than you would as a dividend investor.

However, after you earn over $200,000, suddenly being a dividend investor will end up costing more in taxes than it would being a capital gain investor.

If you are a high-income earner, it is better for you to invest and aim for capital gain because you don’t need to cash out immediately, and the tax rates are lower.

Now if you are retired and you have a lower-income and lower-percentage return, and you’re making around the same for capital gain and for dividend, say 10% for example, then it is better for you to be a dividend investor because you save 3-7% more in taxes.

Now here’s another question: If you become a capital gain investor instead of a dividend investor, can you make a higher return?

Personally, I only see people making around 4-7% a year. Sometimes the dividend can be lower depending on which stock you invest in, by around 2-3%, so it is not a lot of return.

As for capital gain investors, I’ve seen people going from 8-10% which is the market average, to 10-15%. This is a higher range that dividend investments will rarely achieve.

Of course I’m not saying that it’s impossible, but realistically it would be difficult to find dividend investments with a 10-15% return.

Welcome back to the channel. And in this video, we're going to talk about the big question who pays more taxes. Is it the dividend investor that focuses on getting a regular monthly to quarterly income? Or is it the capital gain investor who focused on momentum and hype stocks? And this question who pays more taxes will impact how you plan for retirement. And it'll also impact how you think about the kind of investor you want to beat, because at the end of the day, what you're really maximizing for is the after-tax gain from your investments and doing that. You can grow your portfolio faster, doing that. You can retire earlier and live a more comfortable and less stressful life. So let's get started. So who pays more taxes, dividend investors, or capital gain growth investors. And this video is really a part of a larger series where we look at how to calculate capital gain for us and Canada.

How does trading frequency changes the amounts of taxes? You pay to some tax planning strategies where you can save thousands of cheeseburgers a year. And if you are interested in those other topics, then make sure you go back and watch those videos, or it will be released at a future date. So before we start, I just want to celebrate another case study within investing accelerator, where Mike made 151% from FedEx in 3.5 months using stock options. So congratulations, Mike, that is a fantastic return and good job. And Dexter also sold his FedEx options for 90% gain in seven months. Again, another amazing return. Congratulations Dexter. Now, if you want to learn more on how to become a smarter investor, how to be more confident when it comes to investing and make a higher return long-term then this channel is right for you. So if you tap the subscribe button, then you'll get notified.

When I release future videos around these topics like taxes and motions, how to handle when you're dealing with losses. And so on in terms of the a hundred likes giveaway, I'm currently giving a book called rich dad. Poor dad is one of my favorite personal finance book. And if you liked this video and leave a comment below when you reach a hundred likes, I'll select a winner. So let's look at the scenarios that we'll go through today. Assume you have a portfolio of a hundred thousand dollars and you either make $30,000 in capital gain or $30,000 in dividend. In the first scenario, you have 200 K in income and I'm using 200 K because that is the highest tax bracket you can get. So that makes it simpler. And you make 30 K of dividend or capital gain in a scenario two, I use 70 K of income.

So that means you're kind of in the average salary of Canada. And again, K of dividend or 30 K of capital gain. And in the third scenario is $0 in income. Maybe you're retired. Maybe you just have a lower income with 30 K of dividend or a 30 K of capital gain. And this is the calculator I'm using. And I already took screenshots. So we can just jump straight into the results. So before we do that, we need to understand a couple of concepts. When you're looking at the CRA tax handbook, there are three main important type of dividends. The first one is eligible. Second one is non-eligible and the third one is capital dividend. Now you might be wondering, what are these? Like, why is it so complicated? And how does that impact the amount of taxes you're paying? So we'll walk through each one of them right now, eligible dividends are generally received from public companies.

So that's very simple. If you invest in a stock from Toronto stock exchange, you pay eligible dividends. Non-eligible dividends are generally receive from Canadian private corporations to have paid lower tax rates on a first $500,000 of income. Now, this generally does not apply to you unless you have your own business. When you have your own business, your business profits get taxed, and then you can pay out a dividend to yourself. So that's why it gets at different rates than eligible dividends. So for most of the time, if you don't have a business, this wouldn't apply to you. So we're not going to focus on that in this video. The third one is capital dividend. Now sometimes when a corporation realizes a capital gain, one half of the capital gain is taxable and the other half is not taxable, which I cover in a separate video called capital gain and is added to what known as a capital dividend account.

So this is kind of important because if you sell a property, you pay capital gain. If the corporation sells a property and then pays you dividends, you don't get tax on that dividend because the corporation already paid a capital gain. So that is a very important distinction. And most of the time, when you are getting dividends from public companies, it is going to be the first one it's going to be eligible dividends. And that's what we're going to focus on in this video. Now, just so you know, these are the tax rates. Now these are rule of thumbs and you need to really calculate your specific situation using the CA pass calculator. And I'll leave that in the comment below capital gain in Canada, it's 25% for eligible dividends. It's 39%. It's quite high for non-eligible. Dividend is 45%. And for capital dividend is 0%.

And the reason is because the corporation already paid capital gains tax. Okay, so let's dive into this scenario. Now let's say you have a portfolio of a hundred K and you either make 30% in capital gain or 30% in dividends. Now it's actually makes more sense if I say $30,000 in capital gain or $30,000 in dividends, because it is extremely rare that you can make 30% in dividend. I've never seen it. So just imagine it is $30,000 in capital gain or $30,000 in dividend. We wouldn't look at the efficiency of the capital invested in this video. So we'll just keep the constant in terms of dollar amounts, in terms of the amount of dividends and capital gains, not a first scenario, you're at the highest tax bracket. And in this case, you'll see that on the left-hand side, you get dividend and your total tax bill comes to $77,815.

Wow. Okay. And on the right hand side, your tax bill comes to $75,068. An interesting scenario like this, you actually pay more taxes by being a dividend investor. And that's actually 9% of 30 K. So 9% of your gain is towards taxes. So when you're making a high income, depending on which stage of the career you're in, it's actually this advantageous to you to be a dividend investor, even though a lot of people tell you that you should be a dividend investor, because you're getting monthly income, blah, blah, blah, blah, blah. But the results tells you that you pay more taxes. So you might want to rethink her strategy. If you are making a very high income right now. Now, before I jump on to the 70 case scenario, let me just go back and mention an additional tip when you're looking at capital gain and dividend.

And if you are making a high income, like 200 K, you really need to think, do I need the money right now? And this is a very important concept because if you don't need the money right now, and you are reinvesting the dividend, then why bother paying the tax? Now, when you get dividend each year or a monthly, quarterly, and then reinvest it back into the company, you're you want to invest it. That's a bit counterintuitive because you're paying more taxes and that actually slows your portfolio growth down. So if you are making a high income and you are okay with leaving the money into stock for multiple years, then you should focus on capital gain. Because the analysis I'm doing here is actually just one year. But what you really want to think about is the next five to 10 years, because year after year, if you are a dividend investor, you get tax and tax and tax, whereas capital gain, you keep compounding and you only get taxed at the very end.

And when you exit, assuming you're not a day trader. So when you think about that, it is actually more advantageous to be a capital gain investor. When you are making such a high income, because you don't need the money immediately. So let's jump on to the second scenario, 70 K income with 30 K dividend. And that's when you pay $18,554 in taxes and 70 K income with 30 K of capital gain. And you actually pay $20,500 in taxes. So you actually pay more when you are investing as a capital gain growth investor and how much more, it's really 6% of $30,000, which is $1,946 less in Texas for being a dividend investor. Now, this is actually very interesting. Like why is that? When I first did the scenario analysis, I wasn't really understanding why that is the case, because why does it flip over? And let's look at the third situation first, and this will give you a better idea of what's happening.

Imagine you are retired and now you don't have any pension. You don't have any income and you just get 30 K of dividend or you get 30 K of capital gain. And in this case for 30 K of dividend, you actually pay $0 in taxes and 30 K of capital gain. You actually pay $471 in taxes. So in a way, huh, again, it is better to be a dividend investor by having less income. And when you think about this third scenario, it's important to think about when you need the money. Because when you look at capital gain, it is really what we call paper gain. That means you don't actually get the cash. It's kind of still locked into shares, and there's just a share price going up. But for dividend, it actually gets paid out. So it becomes cash in your portfolio. As you want to take that out and you want to spend it on something you don't need to sell any shares.

The number of shares you still have is the same. So when you are trying to be a dividend or a capital base investor, you need to think about where you are in life. Are you trying to take money out of your portfolio? Are you trying to grow your portfolio to a million dollars? That distinction should push you out of to become a dividend investor or a capital gain investor? Now, here is the answer to the question earlier, why does it flip between being a capital gain investor versus a dividend investor? And in Canada, there is a concept called the marginal tax rates. So that means depending on how much money you're making your tax rate is different. So on the right hand side here, you actually see the table I got for you. And this is for a federal tax where you can see that in the first $49,000, you actually have 0% tax for eligible dividends.

And that's actually quite interesting. And for the first 49,000, you actually have a 7.5% of capital gain tax. Now this is just federal. Remember I said, the rule of thumb for capital gain is around 25%. So you got to combine it with provincial as well. But if you follow this logic, you will see that initially up to $89,000, you will pay more tax as a capital gain investor instead of a dividend investor. And once you get over 200 K, which is 216, K, then suddenly dividend investor will pay more taxes. Now, if you actually look at this carefully after 98,000 dividend investors are ready, pay more taxes. But the scenarios I showed you are actually in here, the red box and this lower red box as well. And that's what I mean. So if you are a high income, earner is better for you to invest and aim for capital gain because you don't need to take it out immediately.

The tax rate is lower, so on and so forth. If you're retired and you have a lower income and a percentage return you're making for capital gain and dividend is around a sane. So let's say 10%, then it's better for you to be a dividend investor because you save this three to 7% in taxes. Now, here is the big question. If you become a capital gain investor instead of a dividend investor, can you make a higher return now for dividend investor? I really see people making around four to 7% a year. Now, sometimes the dividend can be lower depending on which stock you invest in like two, 3%. So it's not a lot of return. And for capital gain investor, I've seen people going from eight to 10%, which is the market average to 10 to 15%. So that range is not something a dividend investor can easily achieve is not saying that is impossible, but it's just difficult for you to find a dividend investments that is 10 to 15%.

Now, some people can do higher risk mortgages that gives you around 10% return. But I would say those people are very rare when it comes to, uh, watching my YouTube channel per se. So if you factor in the incremental return, you get from capital gain versus that dividend return, and you calculate the after tax amount, using the calculator down below in the link, I'll include it. Then you can decide whether you want to be a dividend investor or a capital gain investor. And at this point, I just want to share my vision with you. And my vision for myself is really to make a 30% a year. Actually I've achieved this goal this year. I'm only one month away from December 31st. And I have made more than 30% this year. So far, even though there's COVID. And my journey from zero to 30% a year is really a difficult one.

I learned investing in by myself for eight years. I tried 300 different strategies. I learned programming and investing used to be a black box to me. And I was spending 30, 40 hours a week on learning about investing, reading books, blog posts, watching YouTube videos. And now I'm after investing. And I realize investing is actually very simple. You got to have all the right parts. Now I help people to master investing in four weeks and I transfer all of my knowledge to them so they can become a successful investor as well. And these are the case studies within investing accelerator, where Mike made 151% from FedEx in three and a half months. Dexter made it 90% from FedEx in seven months. And they actually have recorded a video testimonials for me as well. So you can watch that if you want to. And if you want to learn more about my investing strategy on how I use long-term stock options to invest in the markets, then you want to click on the first link below, call it a free webinar, how to get 30% from the markets in 12 months, it should be the very first link.

And when you register for it, you will be taken to a four hour webinar, take your time to go through the webinar. And afterwards, if you're interested, then you can schedule a call with me and we'll have a 45 minute chat and I'll answer any questions you have about investing and we'll map out exactly what you need to do in order to move forward and target a higher return a year. So I look forward to chat with you now, in terms of the next video, I have prepared an interesting topic called are you working too hard as a day trader and paying too much in taxes? So I'll see you in the next one.