Today’s blog will be for Canadian investors. I am going to show you why being a day-trader pays $41,000 more in taxes and what you can do about it.

When it comes to day trading, there’s a certain technique to it, and I am very excited to show you. You are able to take profits within a day or two, and try to earn some quick money.

When you compare that to long-term investing, it’s very slow and there is not a lot of action. With long-term investing you basically get rich very slowly, and that is a major difference when it comes to trading in Canada versus long-term investing in Canada.

WHAT TO EXPECT

By the end of this blog, you will learn why day-trading pays more in taxes, as well as how to save more in taxes.

This post is part of a larger investment tax series which covers other topics such as dividend tax, capital gain tax, and everything tax-related.

In the end you will become more knowledgeable, put more money in your pocket, and avoid the tax-man per se.

The purpose of this blog series is really to help busy full-time professionals like yourself to learn how to invest in the stock market and aim for a higher return.

They are meant to help you save thousands or tens of thousands, maybe even a hundred thousand dollars when you are investing.

DAY TRADING AND TAXES

The first question is, can you use your RRSP and your TFSA accounts to day-trade? The answer is no, very simply. Do not use your RRSP and TFSA to day trade.

Years ago, there were many incidents in which day-traders used these accounts when it first got established and were taxed on it because the CRA went around checking which account has considerable balance, then would review it and take it to court.

If they deemed that you are a day-trader, then they would tax you on it.

DAY TRADING VS. INVESTING

How much tax does a day-trader pay in the US and Canada now?

This concept is actually quite simple. In terms of taxes, it is considered the same as having a second job and therefore equivalent to paying employment income tax.

In other words, you will be taxed at a regular rate.

When it comes to long-term investing, you will be taxed under capital gain, which is only 50% taxable. The rule of thumb is that for capital gain, the average marginal tax rate is around 25%.

In reality, this proportion may fluctuate a little based on your income, but the maximum is capped at 25%.

Here are a series of Scenarios we will go through to illustrate the impact between day-trading and long-term investing, and what you need to do to equate the difference.

- Day-Trading and earning $100K with a $333K Portfolio (30% Return)

- Long-Term Investing and earning $100K with a $333K Portfolio (30% Return, taxed annually)

- What if Day-Trading earns a higher return?

- Long-Term = 10% and earn $100K

- Long-Term = 30% and earn $100K

- What % Return is needed in Day Trading to earn the same amount after taxes?

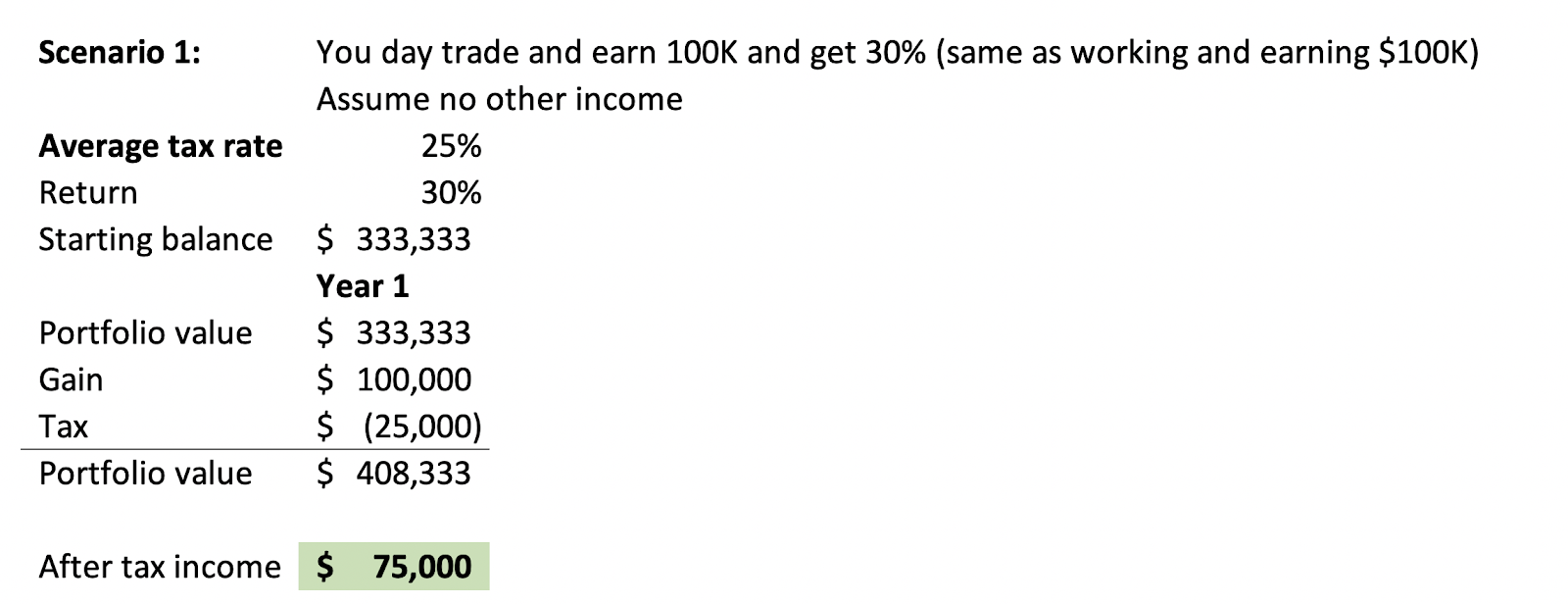

SCENARIO 1: EARNING $100K FROM DAY TRADING - 30% RETURN

In this scenario, you make $100K with a 30% return from day-trading, assuming that you don’t have any other income and you are day-trading full-time.

Assume your starting portfolio balance is $333K and you gain another $100K.

This $100K will be considered employment income on your tax return and you will be taxed approximately $25,000 or 25%, and therefore your income after taxes will be $75,000. Coincidentally, 25% is also the marginal tax rate for capital gain as well.

SCENARIO 2:

EARNING $100K FROM LONG-TERM INVESTING - 30% RETURN

In this scenario, you invest long-term and get a 30% return as well.

You are taxed yearly and technically you can hold your stocks for multiple years and let it grow, but for the purpose of this post let’s just keep it simple and calculate for 1 year.

Your starting portfolio balance is $333K and you get a 30% return but because only half of the capital gain is taxable, you really only enter $50,000 as your taxable income, which means your taxes are significantly lower.

In this case, your taxes are only $7,800 and you can immediately see the difference. Your after-tax income for long-term investing is $92,000 which is a huge increase from Scenario 1.

So how much harder do you need to work to equate the difference?

If you are day-trading with a $300K portfolio vs. long-term investing with a $300K portfolio, the difference is $17,200 as a day trader.

If you need to earn the same pre-tax income as a long-term investor, you need to make an extra $17,200.

SCENARIO 3:

LONG-TERM ETF 10%

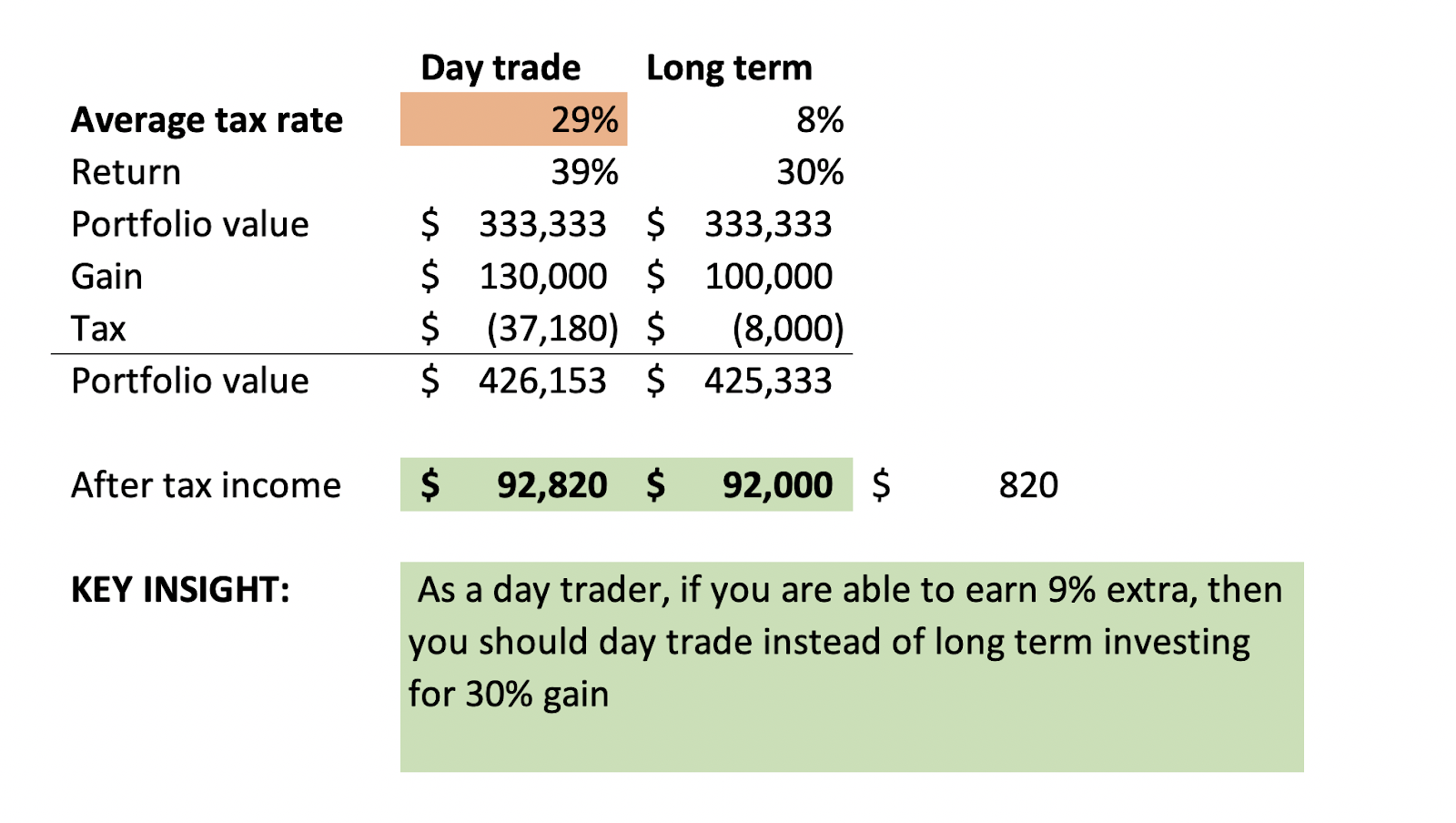

So what if day-trading can earn you a higher return?

For example, if you are investing long-term in only index funds, then your return should be around 10%. That means you need a much larger portfolio to earn $100K.

The reason is because if you want to make $100K and you are making 10% and you need a million dollars, the number has actually increased quite a bit.

If you look at gain, I have kept that constant and the amount of tax you pay as a long-term investor (investing in ETF) is $8,000 which is quite similar to what I showed you in Scenario 2.

In this case, your after-tax income is $92,000.

I played with the left-hand side to try and figure out what the gain that I need to achieve is as a day-trader to equate the difference for long-term investing.

In this case, I figured out that the return % required for day trading is 30%, which is $130,000. With these figures, you will be paying around $37,180 in taxes at an average tax rate of 29%.

After calculations, your after-tax income amounts to $92,820, which is only $820 in difference, or 3% in return.

The incremental difference is not that big of a deal when you’re a day-trader, because I know that traders will sometimes aim for 1% a week or even 1% a day or something along those lines.

In conclusion, I think it is possible for day-traders to be better off when they’re investing and earn higher than a 13% return compared to long-term investors.

However, if you are day-trading right now and earn less than a 13% return then you may be better off putting all your money into an ETF fund.

But of course, if you are learning and your goal is to eventually achieve more than a 13% return, then it might be worthwhile.

SCENARIO 4:

LONG-TERM INVESTING 30%

How much return would you need to earn as a day-trader to match the same amount as a long-term investor with 30% return?

In this scenario, the long-term investor remains constant to the previous scenario.

They pay around $8,000 in taxes, the after-tax amount is $92,000 and the portfolio balance is $333,000.

After playing with some calculations I found that the percentage and return needed is actually 39% in order to make the same amount after deducting taxes.

In this case, you gain will be around $130,000 and the tax is $37,000 which is the same as the previous case. I think a 9% incremental increase is actually quite significant, so with a 39% return that means you need to make approximately a 3.5% return per month which I think is achievable.

However, if you are able to invest long-term and get 30%, then why invest all this time into becoming a day-trader?

Of course, everyone is different and has a different strategy, but you just need to factor in the amount of time required for each method.

As a day-trader, you might be putting in 30 to 40 hours a week which is fairly reasonable, whereas a long-term investor may spend only 1 to 2 hours per week.

BONUS SCENARIO 5

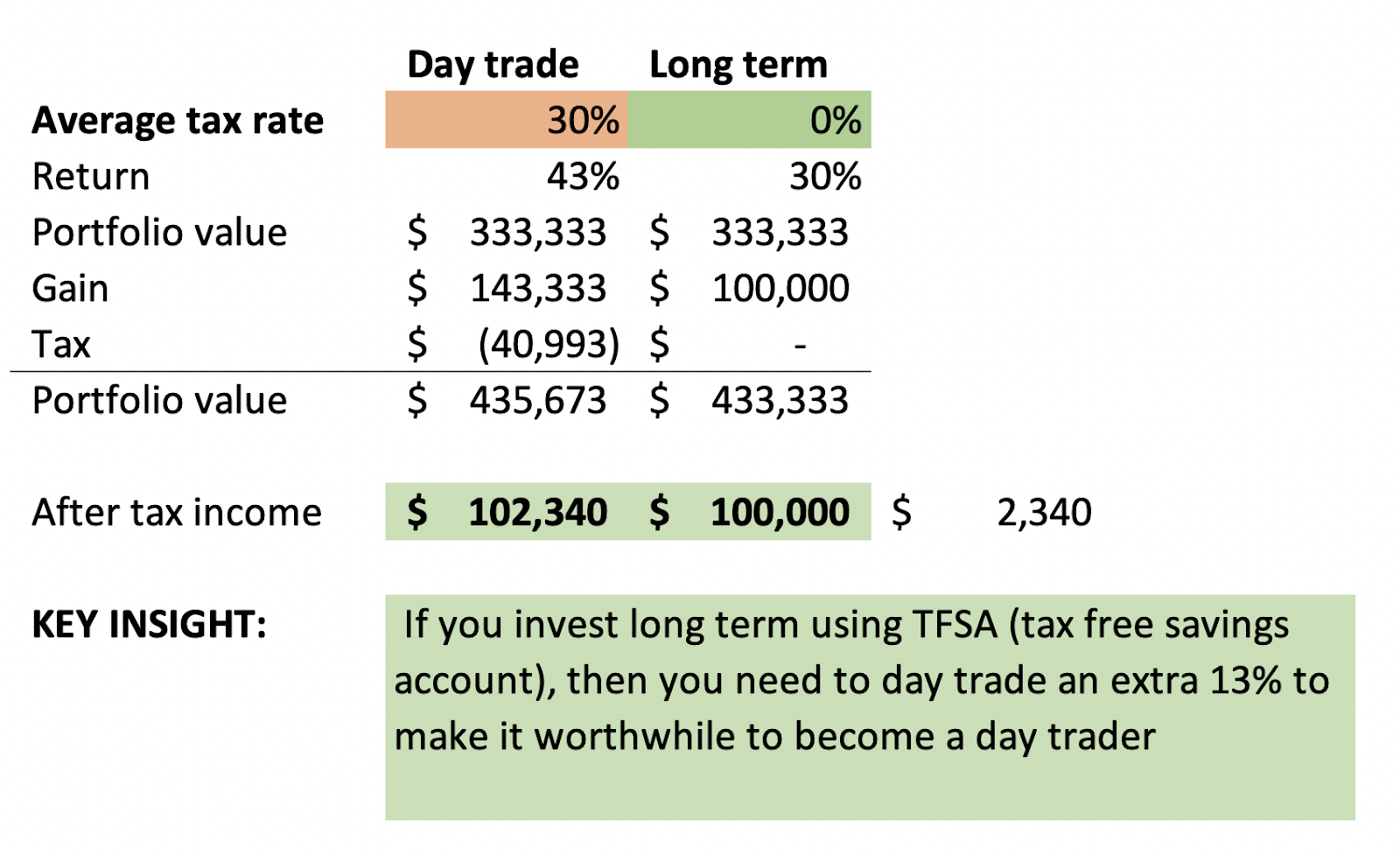

USING TFSA TO INVEST

What happens if you use TFSA accounts to invest in the market?

In this case, you wouldn’t actually be able to use TFSA accounts to day-trade, but you can use them for long-term investing.

This will give you a significant edge because you don’t pay any taxes on your TFSA account, so I put 0 in the taxes section. This means that your after-tax income is $100,000.

If you want to achieve the same return using day-trading, then you would need to earn around 43% in return to get the same after-tax income of $100,000.

So now you can visually see that you would need to work 33% harder to earn the same amount as a day-trader, and you also need to spend 30 to 40 hours in front of the screen.

That is quite a bit of manual work and it can be energy-draining as well. When you are evaluating whether it is worth it to be a day-trader, that is what it really comes down to - whether the ultimate results will align with your goals and lifestyle.

In this video, I'm going to show you why being a day, trader pays $41,000 more in taxes and what you can do about it. And when it comes to day trading, there's a certain throw to it. It's exciting. And you take a profit within a day or two, it try to make some quick money. And when you compare that to long-term investing, it's very slow. There's not a lot of action. And basically you get rich slowly, and that is a major difference when it comes to a trading in Canada versus long-term investing in Canada. And by the end of this video, you'll learn why a trading pays more in taxes and $41,000 more as a long-term investor, you'll learn how you can save more taxes. So then you can earn a higher return we'll file putting in more effort. So this is really a part of a larger investment tax series, where we cover dividend tax capital, gain tax, everything PAX related.

So then you can become more knowledgeable and put more money in your pocket and basically avoid the tax man per se. And the purpose of this channel is really to help busy full-time professionals like yourself to learn how to invest in the stock market and aim for a higher return. These videos are meant to help you to save a thousand, 10,000 or even a hundred thousand dollars when it comes to investing. So in terms of the a hundred likes giveaway for this week, we have got a new book I'm reading called factful and Ashley have it with me here. And this is the book. And so far is actually quite interesting. It talks about income inequality and why our understanding of the world is wrong. And there's actually a 10 question survey within the book. And I got, I think maybe five to seven of them wrong on my first try.

So if you are interested in reading this book as well and expand your knowledge, then you can click like on this video and leave a comment below and I'll select a winner once we reach a hundred likes. So in terms of investing a celebrator, I just want to celebrate another successful story where Adrian sold his corny G L w options for 172% return and format. That is pretty amazing. And his courting position has an average return of 128%. And he also sold part of his PLC position, which is using stock for 40% gain. So that is pretty amazing as well. So congratulations, Adrian. And finally for Mike, he also sold half of his MSI stock for 55% in four months. Uh, so that is very amazing as well. So right now for investing accelerator, we are looking for 15 individuals to teach them how to invest.

Even if you don't have a financial background, there's more details at the end of this video. So day trading and taxes. So the first question is really, can you use your RSP and your TFSC accounts today day trade? And the answer is no very simply do not use your RSP and key FSA to day trade because there are a lot of cases where a day trader is actually did that many years ago when it first started established and eight got taxed on it because basically CRA will go around and he will see which account has a lot of balance and they will review and it will bring you to court. And if they deemed that you are a day trader, then they would tax you on it. So the question is how much tax does a day trader pay in us and Canada now for day trading is actually quite simple.

It's the same as having a second job is the same as paying employment income tax. So you're going to be taxed at the regular rate. And when it comes to long-term investing, you will be taxed under capital gain, which is only 50% taxable. So the rule of thumb is that for capital gain, the average marginal tax rate is around 25%. Now, in reality, it might fluctuate a little bit based on your income, but the max it goes is 25%. So here are a couple of scenarios that we'll go through and we'll dive into to understand what is the impact between day trading and long-term investing and what you need to do to basically equate the difference. So, first we're going to look at day trading and earning a hundred K with a 330,000 portfolio. So what that means is you're getting 30% return on 333 K, which is a hundred thousand dollars in gain.

Let me know if that's not clear. So basically you made a hundred thousand dollars in income from day trading. Now, the second scenario is that if you are, long-term investing and you're earning a hundred K using a 333 K portfolio as well, again, 30% return tax yearly. So technically you can hold on to it and let it grow for multiple years. But in this case, we'll keep it simple and look at one year. The next question is, what if they trading can get a higher return? You know, if you're your long-term investing only in index fund, then you should get around 10%. So that means you need a much larger portfolio to get a hundred K, but we'll keep that constant. So what is the return day trading you need to get to get the same after-tax return. And finally, what happens if you make 30% as a long-term investor and what is the percentage day trading needs to get in order to compensate for the tax?

And that's going to be important because if you're not able to meet the recurrent percentages that I'm about to tell you, then maybe it's not worth it to day trade. So let's start with the first scenario. So when you day trade and you make a hundred thousand dollars and you get 30% return, and I assume you don't have any other income and you're full time on day trading. So what that means is that your starting portfolio balance will be $333,000, and you gain a hundred thousand dollars and that will be attacks of $25,000. So you would put this a hundred K as your employment income on your tax return and you get tax approximately $25,000. So that means your after tax income is actually 75 K. So it was pretty straightforward is 75 K. Now, coincidentally, this is Ashley, the marginal tax rate for capital gain as well and a double-check to make sure that is not the case.

It's not a calculation error. So now first scenario two, you invest long-term and you get 30% return as well. So your starting balance is 333 K you get 30% return, but because only half of the capital gain is taxable. You only really put $50,000 as your taxable income, which means your taxes is a lot lower. So it's only $7,800. So immediately you can see the difference. You went from paying $25,000 to $7,800. And your after tax income for long-term investing is $92,200. Wow, that's a huge increase. So that means how much harder do you need to work to equate the difference? So if you're a day trading with a 300 K portfolio, versus your long-term investing with a 300 K portfolio, the difference is $17,200 as a day trader. If you need to earn the same pretax income as a long-term investor, you need to make an extra $17,200.

So what about ETF? If you are only getting around 10% for ETF, then you need to use a much bigger portfolio. And the reason is because if you want to make a hundred K and you're making 10% and you need a million dollars, this number has actually increased quite a bit. If you look at the gain, I have kept that constant and the amount of tax you pay as a long-term investor, investing in ETF, it's $8,000, which is very similar to what I showed you earlier. And in this case, your after-tax income is $92,000. So then I was playing with the left-hand side and trying to figure out what is the gain I need to achieve as a day trader to equate that difference because day trader are taxed differently than long-term investors. Now, in this case, I have figured out the amounts to be around a 30% return, which is $130,000.

And in this case, you will be paying around $37,180, which is an average tax rate of 29%. And after that, when you calculate the math, then it gets pretty close. The after tax income is 92,820, which is only $820 in difference, 3% return. That incremental difference is actually not that big of a deal when you're a day trader, because I know the traders will sometimes aim for 1% a week or even 1% a day or something along the lines of that. So I think it is possible for day traders to be better off when they're investing and get higher than 13% return compared to long-term investor. So if you are day trading right now, and you get less than 13% return, then you're better off just putting all your money in the ETF fund. But of course, if you're learning and your goal is to eventually achieve more than 13% return, then it might be worthwhile.

Now the fourth scenario is really long-term investing gets, gets 30% return and how much return does the day trader need to make? Now, in this case, this is the same as before where I'm paying around $8,000 in taxes. And after tax amount is $92,000 of my portfolio balances to 333,000. And for day trader, I was playing with the percentage and the return is actually 9% is what you need to make the same after-tax amount. So in this case, your gain will be around $130,000 again. And in this case, the tax is 37,000, same as before. And the difference is 820 as well. So that is really the key difference. And then I was thinking to myself, wow, a 9% more incrementally compared to getting 30% long-term is actually quite significant. So with a 39% return, that means you need to make approximately three and a half percent return a month, which I still think is doable.

But if you are able to invest long-term and get 30%, then why investing all this time to become a day trader? Now, of course, everyone is different and everyone has a different strategy, but you just need to factor in the amounts of time. You need to put in as a day trader versus a long-term investor. So for a day trader, you might be putting in 30 to 40 hours a week, which is fairly reasonable. Whereas long-term investor might be one to two hours a week. Now I actually got a fifth scenario for you and a bonus scenario. And the question is what if you use TFSC accounts to invest in the market. Now, in this case, you wouldn't be able to use TSA to day trade, but you can use TSA for long-term investing. This will give you a significant edge because you don't pay any taxes on your key FSA account.

And in this case, I've put it at zero. So then that means your after-tax income is a hundred thousand dollars. And if you want to achieve the same return using day trading, then you need to get around 43% return in order to get the same after-tax income of a hundred thousand dollars. So you can see that you need to work, you know, 33% harder when it comes to day trading, and you also need to spend 30 to 40 hours in front of the screen. So that's quite a bit of manual work and it can be energy draining as well. So when you are evaluating, whether it is worth it to be a day trader, that is what you really need to look at is the ultimate results. And whether it is able to fulfill your life's demands and your goal. Now, the vision for myself is really to make 30% a year being a long-term investor.

I've done it for the last five years, pretty successfully. And I just want to share this knowledge with you as well. So I have prepared a four hour training that is made for a full-time professionals or a retiree with no financial background. And you want to manage your own portfolio. You want to learn how to get 30% a year. And if that is the case, then you can attend the free four hour training here. The link is the first link in the description. And if there are three reasons why you might want to get this training, and the first reason is you want to learn how I made 500% in the last five years. So that's an average of 48% a year, and you'll also learn how I help over a hundred people without a financial background to master investing. So there's really no reason why you wouldn't be able to master it.

If you put into time and the effort and attending this four hour training is probably better than going through another 100 videos on YouTube, which can be time consuming. And this training is really condensed, simple, and actionable. So you can get the free training and description. So I'll see you inside the webinar. And for my journey to 30% is really a difficult one because it took me eight years to get there. And initially I was making a negative return, so less than 10%, and I have very low confidence. I didn't know what, what I was doing. I didn't have a mentor. I was basically just doing random things, testing different strategies, programming different strategies until I figured it out. And now I only have one simple investing approach where I aim for 30% a year. And my goal is to teach more people how to do that as well.

So here are some examples I talked to you about earlier today, for example, Adrian making 172% from corny 40% from PLC in a couple of months, Mike made 55% from MSI in four months. And right now I'm looking to help 15 more people to master investing this month. So if you're interested, go attend to free training first so that you have a complete understanding of what I do afterwards. So you can schedule a call with me to have a chat, and I'll see you on the call in the next video I'm going to talk about, should you be concerned that investing frequently will increase your taxes? This video idea came from Warren buffets where many years ago, he said that you should be aware of taxes. You also should be aware of transaction costs. When it comes to investing, we're going to do a couple of models together to figure out whether there is a significant impact when it comes to transaction costs and also taxes. If you are investing frequently versus holding for five to 10 years. So if you are a long-term investor and you want to minimize your taxes, then the next video is definitely for you.